|

Perspective

By Rich Checkan

Have you visited our new website lately? More on that in a bit…

So far, 2024 has not been kind to gold and silver. Gold is down a little over one percent. Silver is down nearly six percent.

Both monetary metals were taken to the woodshed last week by the one, two punch from the Federal Open Market Committee (FOMC) and the Bureau of Labor Statistics (BLS).

Last Wednesday, the FOMC had their first interest rate decision meeting of the year. They took no action… leaving interest rates unchanged. But the words from Chairman Jerome Powell afterwards in the Question-and-Answer session dampened the hopes of equity and precious metal investors alike.

Mind you, none of this should have been a surprise at all.

Chairman Powell and the other Fed Governors have been clear and on point ever since December when they all but promised multiple interest rate cuts this year. Since then, they have all said the cuts would come later in the year IF inflation comes down and the economy remains resilient.

Of course, the markets heard what they wanted since December… hoping against hope for an interest rate cut as soon as March. Some actually believed the FOMC would cut interest rates in January!

They were clearly bad listeners.

Chairman Powell reiterated his position of “higher for longer” last Sunday in an interview on 60 Minutes.

Investors hopeful for lower interest rates were dealt another blow last Friday from the Bureau of Labor Statistics. The BLS reported 353,000 new non-farm payroll jobs created… nearly double what the markets expected. That kept the unemployment rate steady at 3.7%.

So, with inflation holding steady or ticking slightly higher, and with the labor market holding steady, Chairman Powell and the FOMC have no compelling reason to rush into interest rate cuts.

And that did not sit well with investors. Equities have pulled back since. Precious metals have pulled back as well.

Volatility is alive and well.

Rainbows and Unicorns

If you buy into the headlines and voraciously drink in the data reported dutifully by the mainstream press, you no doubt believe the economy is sailing along as smoothly as can be.

Virtually nobody is unemployed, yet we keep hiring new workers at a feverish pace. Economic growth is exceeding expectations. Consumer spending is strong, but inflation seems to remain in check.

It is indeed the best of all worlds.

Or is it?

Let us start with the jobs numbers. Have you ever noticed how loudly the payroll numbers are reported… but how quietly they are retracted?

Everyone knows we added an extraordinary number of 353,000 jobs last Friday. Does anyone know about the downward revisions whispered quietly after the fact?

I have not seen the December revision yet, but 71,000 job gains in October and November were corrected… quietly… without any fanfare… without a single headline. Let’s not even talk about the gross disparities between the “establishment survey” and the “household survey” conducted by the BLS.

The “establishment survey” is what is reported as non-farm payrolls. Yet, the “household survey” – which is used to calculate the unemployment figures - tends to be more accurate.

According to Schwab, since April 2022, the difference between the two numbers is massive. The “establishment survey” reported 5.8 million new jobs created. Over the same period, the “household survey” reported 3 million new jobs created.

The “establishment survey” is twice as optimistic as the “household survey.”

In addition, the caveats in these numbers are seldom discussed. The two most important caveats are the increases in both the number of people who hold two jobs because one job is not enough to support themselves and their families and in the number of people who hold a part-time job but would much rather hold a full-time job if one were available.

These two rising numbers suggest that wages have not been keeping up with inflation for some time, and the quality of positions available is not adequate.

All I care to say about economic growth is that it is coming from the wrong sectors. Growing government spending is not a sustainable sector of growth for any economy. Creating money out of thin air and giving it to individuals to spend has a two-fold increase on Gross Domestic Product (GDP), but what is created for the economy?

The last point I would like to make is nothing new. I have been harping on this for the past couple of years now.

Consumer spending is not a sign of household balance sheet strength. Rather, it is a cry for help in difficult economic times.

Spending has been up over the past year because we are buying the same things we bought – the things we need – a year ago. The difference is they all cost more this year due to inflation.

The rate of inflation is easing, but prices have been steadily going higher for years. And they are still going higher now… at double the Federal Reserve’s target inflation rate.

This next part is concerning. Credit card debt is increasing. Credit card interest rates have risen to over 20%. Those carrying balances month to month on their credit cards are on the rise. Credit card delinquencies are on the rise.

I see very few rainbows and not a single unicorn. Sorry.

Take Action Now

Many investors are taking a wait and see attitude.

They feel gold and silver prices are high. They are hoping for lower prices before Chairman Powell and the FOMC start raising rates (if they do) later this year.

I think that is a mistake.

Things are not as rosy right now as the headline numbers suggest. As Adrian Ash suggests, we could be on the verge of even more dire economic circumstances as bad commercial real estate narratives start to unfold.

And those waiting for gold prices to move should listen to Rick Rule’s cautionary comments in my short video interview with him. I think you will be surprised to hear Rick’s favorite resource for 2024!

The economy is not strong right now. Gold and silver prices are not high right now.

You have an alternative to the narrative of the mainstream press. Start with our new website. You will see a ton of information that you won’t necessarily hear from the talking heads on television.

And now you can buy right online as well.

Visit www.assetstrategies.com today to see what is available.

Of course, you can still call us at 800-831-0007 or send us an email to set-up a consultation. Let us help you Keep What’s Yours!

—Rich Checkan

Editor's Note: Rick Rule is president and CEO of Rule Investment Media. He began his career in 1974 in the securities business and has been involved in it ever since. He is known for his expertise in many resource sectors, including agriculture, alternative energy, forestry, oil and gas, mining, and water. Mr. Rule is actively engaged in private placement markets, through originating and participating in hundreds of debt and equity transactions.

Feature

Q&A with Rick Rule

As we begin the new year, I thought it would be worthwhile to share a brief conversation with you. I recently spoke with Rick Rule of Rule Investment Media and formerly of Sprott U.S. Holdings. Rick truly needs no introduction as a 50-year veteran of natural resource and precious metals landscape.

Rick’s insights into those markets for 2024 are absolutely worth the 25-minute listen. You will undoubtedly be surprised at his favorite resource for 2024.

Enjoy the brief interview, then, be sure to register for Rick’s Natural Resource Symposium at The Boca Raton Resort in Boca Raton, FL, July 7-11.

I will be there with Rick amongst a Who’s Who of natural resource experts, analysts, and companies.

If you want to make sense of what is going on in these markets, this is a can’t miss event.

See you there…

Click to view video.

Editor's Note: Omar Ayales is the Senior Trading Strategist & Editor at GCRU (Gold Charts R Us). If you have any questions, you can reach him at oayales@adenforecast.com or visit www.goldchartsrus.net.

Hard Stuff

Sticky Inflation

By Omar Ayales

In December, the Federal Reserve cracked open the champagne, celebrating its victory against inflation. Back then, Powell called a peak in the Federal Funds Rate, providing an updated dot plot anticipating rate cuts during 2024.

Financial markets rose with strength; assets rose to new highs. And just when the party was getting hotter, robust economic data showing a solid labor market and a confident consumer in the U.S. reminded everyone that the inflation genie might not have been put back into its bottle yet.

The Fed’s Powell gave a press conference and an interview on 60 Minutes. He made sure to let everyone know the Fed was not on a preset course to cut rates and that, although Powell did signal peak rates last December, the Fed isn’t ready to start cutting rates just yet.

Powell acted quickly, communicating as efficiently as possible without creating distress, fear, uncertainty, or doubts as to the direction of monetary policy. But the damage was already done. Financial markets were paying attention, and asset values across the board were shattered.

It’s bearish for gold as the expectation of long-term positive real rates takes up a more significant share of overall haven demand. By real rates, I mean the interest rate on a benchmarked yield, such as the U.S. 90-day T-bill rate, less the inflation rate (as measured by the CPI or the PCE). This means positive inflation-adjusted returns on benchmark (haven) treasuries put downside pressure on gold.

It’s bullish for the U.S. dollar index as it has been rising with interest rates since May 2021. The U.S. dollar index’s recent break-out rise above 104 re-confirms support above 100 and opens the door for a continued rise to the Oct 2023 highs near 107.

A rising U.S. dollar index could continue to put downside pressure on commodities and currencies. However, it is yet to be seen if the dollar has the resilience to break above its next resistance and confirm a renewed leg-up rise.

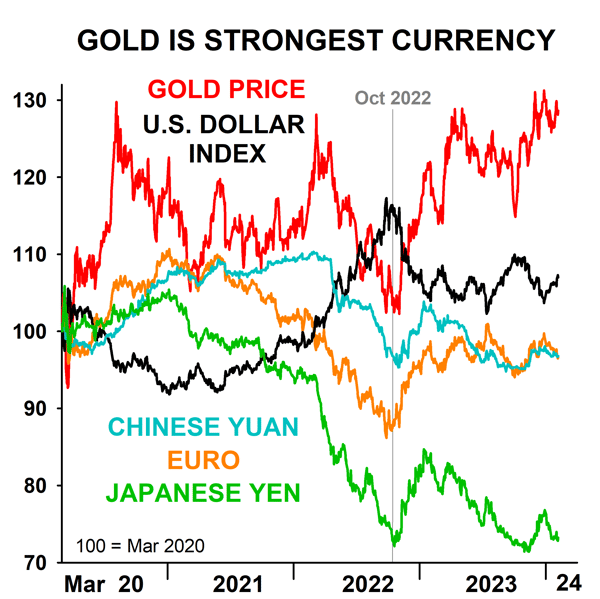

The U.S. dollar index could remain the strongest currency and most influential on a relative basis, particularly as China continues to sputter in its economic recovery. However, compared to gold, gold will likely continue to outperform the dollar longer term.

Notice this chart, a comparison between major global currencies and gold since the depth of the COVID-19 crisis, indexed to 100 to measure relative strength. Notice that gold has been the strongest, much more robust than most currencies, including the U.S. dollar index.

Given the inevitability of monetization of debt, global fragmentation, and war, gold will likely remain on an upward path, possibly outperforming international currencies and other safe havens.

Consider gold tends to move in cycles. One of the cycles that identifies the intermediate move in gold is the ABCD cycle. According to this cycle, gold is currently in a ‘B’ decline, a gut-wrenching decline that tends to be short-lived. We’re about halfway through with some more to go. Most importantly, it precedes a ‘C’ rise, the most vital up move in gold.

A break above the recent peak and resistance area near $2,075 would mark the end of gold’s ‘B’ decline and the start of its ‘C’ rise. An up move that could last about nine months and rise approximately 25% from the ‘B’ decline low.

The time to buy and accumulate gold, silver, and the miners is now.

Editor's Note: Adrian Ash is director of research at BullionVault, the world-leading physical gold, silver and platinum market for private investors online. Formerly head of editorial at London's top publisher of private-investment advice, he was City correspondent for The Daily Reckoning from 2003 to 2008, and he has now been researching and writing daily analysis of precious metals and the wider financial markets for over 20 years.

The Inside Story

Gold Price Rallies from Powell's Fed 'Bombshell' as CRE Debt Iceberg Hits Banking

By Adrian Ash

The gold price rallied $10 from another drop to $2,030 per Troy ounce on Thursday in London, again erasing the drop made overnight when US central bank chairman Jerome Powell said the Federal Reserve won't cut Dollar interest rates in March as financial markets had expected, even as fears over bad debts in US commercial real estate hit banking stocks.

Asked whether falling inflation could permit a rate cut after the Fed held at a 2-decade high of 5.50% on Wednesday, "I don't think it's likely that we'll reach [that] level of confidence by the time of the March meeting," Powell replied.

"I don't think that's the base case."

"That's the bombshell and all that matters," said Swiss bullion refining and finance group MKS Pamp's Nicky Shiels in a note Thursday morning.

"With one out-of-character quip, Powell put any hopes/bets of rate cuts in March to bed."

Further ahead, says Jonathan Butler – head of business development at Japanese conglomerate Mitsubishi's precious metals division – "Geopolitical tensions as well as speculation over the outcome of the US election should keep gold well supported as a risk hedge.

"[But] if the actual pace and magnitude of Fed rate cuts ends up undershooting expectations, then gold may be in for a downwards correction as the year progresses."

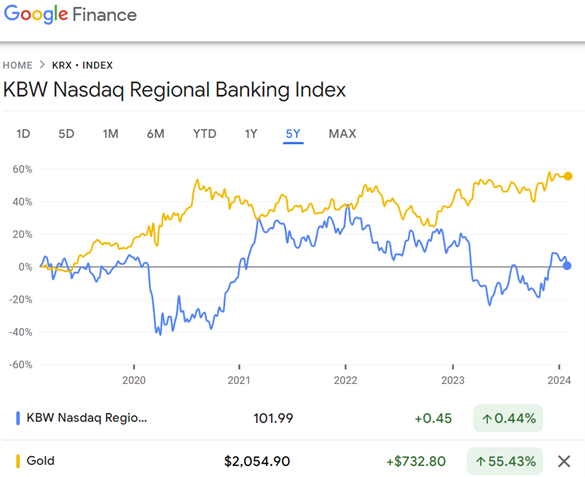

Powell's comment came amid a 37.6% plunge in the stock of New York Community Bancorp (NYSE: NYCB), the $4.7 billion lender which last spring bought some "strategically and financially attractive assets and liabilities" from Signature Bank, the crypto-focused bank whose 'concentration risk' saw it fail during the spring 2023 turmoil in regional US banking shares that started with the collapse of Silicon Valley Bank, then spurring fears of a US recession and expectations of steep Fed rate cuts which never materialized.

NYCB's drop on Wednesday saw the wider KBW index of US regional banking stocks sink 6.0% on Wednesday, its worst 1-day drop since that 'mini crisis' of 10 months ago.

"The official Federal Open Market Committee statement erased language it had used previously that it held a bias toward more hikes," notes Bloomberg columnist John Authers.

Comparison with the Fed's previous policy statement also shows it put a red line through December's assertion that "the US banking system is sound and resilient".

Shares in Tokyo's Aozora Bank (TYO: 8304) today dropped by 1/5th after it warned of losses on US commercial property investments, and Deutsche Bank (FRA: DBK) has "more than quadrupled its US real estate loss provisions to €123 million ($133m)," says Bloomberg. But shares in Germany's biggest bank today jumped 5.5% in Frankfurt after its 4th quarter results "smashed expectations" with a net profit of €1.3bn for October-to-December, plus news of an "efficiency program" set to cut 3,500 jobs.

"No reaction in gold as yet," says a note from bullion analyst Rhona O'Connell at brokerage StoneX, looking at how Aozora's shares fell after NYCB. "But I still fear that this news could be the tip of the iceberg, especially with regard to commercial real estate in the United States.

"Buried in the Minutes of the December FOMC meeting," O'Connell says, was a note on how "delinquency rates on non-farm non-residential CRE bank loans rose further in the third quarter...The large volume of loans scheduled to mature over the next few quarters suggested that delinquencies would likely surge again."

Betting on March's Fed rate decision today put the odds of a cut down at 35.5%, slumping from yesterday's 54.5% to the weakest since end-November and sharply in contrast with the peak of 90.2% hit at the end of December, when the Dollar gold price ended the week, month, quarter and year with a new all-time closing high of $2062 per Troy ounce.

Betting on the Fed's December 2024 decision, however, has barely moved, with the market still expecting steep rate cuts by year-end and the consensus forecast edging only 3 basis points higher from yesterday's near-3-week low of 3.88% according to derivatives exchange the CME's FedWatch tool.

Silver also rallied on Thursday, but unlike gold it failed to regain yesterday's level, trading 20 cents lower for the week so far at $22.75 per Troy ounce.

Creditors of failed Chinese property development giant Evergrande are likely to lose most of their investments, Bloomberg reports today, as its liquidators struggle to sell real-estate assets in a "slumping market".

|