|

Perspective

By Rich Checkan

Last month, I started this column lamenting how bad September was for gold and silver prices.

October was the opposite of September. Gold found its way briefly above $2,000 per ounce, and silver found its way above $23 per ounce.

What happened? Is it sustainable?

As always, I have some thoughts, and I am in the Big Easy at Brien Lundin’s New Orleans Investment Conference to share those thoughts with the investors in attendance. And of course… with you here as well.

What Happened?

As Glen O. Kirsch would quip when the price went up, “There were more buyers than sellers.”

However, who is doing the buying is critical information.

As I’ve mentioned several times this year, central banks have been buyers of gold for the past 13 years. Last year, central banks bought more gold than at any time previously in history.

The start of this year saw that demand continue. Central banks bought more gold in the first quarter of 2023 than they did in the first quarter of 2022’s record year.

But, since then, central bank buying has tapered off. It is said to be down 27% from last year’s blistering pace, but the central bank buying has been significant all the same.

Surveys suggest the central banks are buying…

- To preserve purchasing power.

- To hedge against inflation.

- To protect against changes in the global monetary system.

- And to shift reserve assets from U.S. dollars to gold.

Since Hamas attacked Israel on October 7th, new buyers have emerged… crisis speculators. These speculators have moved the prices on gold up through $2,000 and silver above $23.

Fears of escalation of fighting in the region continue to drive this trade despite short-term reprieves for profit-taking or for Federal Reserve follies.

Is It Sustainable?

History suggests crisis-driven price hikes are not sustainable.

I remember clearly the price action of gold when the planes hit the World Trade Center on 911. Gold spiked… $50 per ounce in intraday trading. Given gold started that day at $270 per ounce, the spike was significant.

Within a month, the price was back down where it began that fateful day.

Crisis investing, in my humble opinion, is not sustainable.

Central bank buying can be. At least, it can give the market some much needed downside support. In fact, it has been doing just that for some time now. It is the reason gold has held up so well despite treasury yields rising from 0.11% to over 5% in the blink of an eye.

However, central bank buying and crisis speculation cannot take to the lofty levels that many hard money investors expect to see in this current bull market.

To get there, investors need to get into the act.

The Missing Piece

Investors are the missing piece.

Sure, they flooded into the market in the first quarter. Fears of the extent of the banking crisis drove them to gold.

But in the second quarter, they believed the banking crisis was over. I personally believe the crisis is just pausing, but investors felt safe and secure… and they stopped piling into gold.

All along, we’ve seen well-healed investors buying. They aren’t typically choosing between buying gold or buying necessities like food, shelter, and gas.

Main street investors are making those judgements right now. They’ll put those necessities on a credit card (and boy have they been), but they won’t make an investment into gold on a credit card at these high interest rates.

Since they can’t just refinance and take cash out of their home equity, gold purchases are on hold. With home finance rates at 8%, that simply is not an option for them.

Americans are struggling. What the Fed interprets as higher consumer spending and a resilient economy is really consumers buying necessities, on credit, at higher prices… thanks to the inflation of the past couple years.

The Federal Reserve’s interest rate increases are breaking the banks and breaking the backs of the middle class. Until things change, I don’t see the move to the next plateau for gold and silver prices.

What Will It Take, And What Should You Do?

For gold prices to catch fire sustainably, I believe we need to see a sustained pause in interest rate increases and the eventual reduction in rates.

Make no mistake. It is coming.

The Federal Reserve is at the end of its rope. They cannot go meaningfully higher with rates, because the $33.5 trillion debt cannot be serviced as is. And we are already seeing the appetite for U.S. debt drying up. It’s simply getting too risky with no signs of Congress cutting spending and becoming fiscally responsible.

Right now, Federal Reserve Chairman Jerome Powell is hoping strong words will buy some time. That’s all he really has. He is out of ammunition.

Knowing that, take this time, as you are able, to shore up your allocations to gold and silver.

Don’t chase the gold price higher. But don’t shy away from gold at these levels either. Work your plan. Fill your allocation.

“If you are buying gold for the right reason, there is no such thing as the wrong price or the wrong time.”

Let us help you Keep What’s Yours… now.

Send me an email today. Give me a call (800-831-0007). Come see me at Joel Nagel’s 27th President’s Week Annual Conference.

Make a plan. Work your plan. Own gold now.

Over time, measured in mismanaged fiat U.S. dollars (or in yen, euro, or pounds for that matter), the price is going higher. If that is something you doubt, simply zoom out.

Look at gold’s body of work over the past century… then, give me a call.

—Rich Checkan

Editor's Note: Bill Bonner is the Founder of Bonner Private Research and owner of the Agora Companies. This article was originally published by Bonner Private Research on October 26, 2023. You can subscribe to Bonner Private Research here.

Feature

Joyride to Catastrophe

By Bill Bonner

The bond rout deepens, the empire recedes and your fellow readers weigh in on what comes after the US Dollar...

"Geopolitical tensions are highly elevated and pose important risks to global economic activity."

~ Jerome Powell, last week

We have no reason to abandon our hypothesis. The financial world shifted in the summer of 2020. Thenceforth, the last shall be first...

We’ve seen how the bond market has been turned upside down, with the world’s safest credit – the US Treasury 10-year bond – losing 40% of its real value. What we haven’t seen is a massive selloff in the stock market. Instead, equity values are being chipped away by inflation.

And while bonds should bounce…inflation might take a break…and stocks might go up…the Primary Trend will probably be with us for many years – bond yields up, stocks down, with inflation going up and down, but not going away.

The Spiral Effect

This new Primary Trend will require large-scale adjustments, including erasing trillions of dollars’ worth of ‘investments’ that can never pay off. That is just the way of the world…nothing to worry about, provided you’re on the right side of the adjustments…and the authorities don’t make the situation worse.

But that is exactly what they are doing. Rather than cut back on spending and borrowing – Congress continues its joyride to catastrophe. Business Insider:

Treasury bond supply could soon hit record levels as unsustainable deficits and high rates create spiral effect, Bank of America says

"Higher interest rates will likely have a meaningful impact on deficit spending and result in larger UST issuance, creating a spiral effect. Rates will have to materialize more than 100bps below forwards for costs to not rise materially as a share of GDP," the analysts wrote. "A daunting supply picture becomes even more challenging given the backdrop of higher financing costs."

With the $1.7 trillion deficit of fiscal year 2023 topping expectations, BofA adjusted its outlook for future years: between 2024 and 2026, deficits will steadily climb from $1.8 trillion to $2 trillion.

Meanwhile, net interest payments will account for an increasing share of GDP, climbing to a record 3.5% in 2026.

Which brings us to our theme. It’s the ‘more to the story’ we’ve been hinting at. Several intriguing and dangerous trends are afoot; other ‘primary trends.’

Bombs Bursting in (their) Air

Already, the US firepower industry is doing all it can to keep the killing going in the Ukraine and Israel. Last year, Putin and Zelensky were reportedly ready to reach a negotiated settlement. The US and Britain insisted that the war continue. And last week, Brazil proposed a ceasefire in Gaza. Most of the UN was in favor. But the US vetoed it. And here comes Joe Biden with a request for $105 billion more of firepower.

The mistake is so obvious, it must be no mistake at all. In WWI, by 1916, England, France and Germany were already worn out from two years of war. Left alone, they would have had no alternative but to work out a peace settlement. Enter the US with an almost inexhaustible supply of new money, soldiers and delusions…and the war continued for another two years – with perhaps 10 million more deaths, leading to the Bolshevik Revolution in Russia and the rise of Nazism in Germany.

Today, without US support, the guns would probably soon stop blazing in the Ukraine and in Israel, too.

But the situation is also fundamentally different. The US was the young, rising power of the 20th century. Now, by our reckoning, it is a declining one.

A man of a certain age fears losing his masculinity. He colors his hair. He takes the ‘blue pills.’ He ditches his old wife and takes up with a chorus girl. Trying to deny the inevitable, he risks making a fool of himself…and a disaster of his life.

Geriatric Caesar

A great empire has its night sweats and daylight dreads as well. Its aristocrats and political heavies fear being upstaged, outgunned, and overshadowed by an upstart competitor. It sends out its warships…it offers its bribes and payoffs…it builds up its garrisons – like the poor Roman limitanei shivering on the banks of the Danube or poor Charles Gordon starving in Khartoum while waiting for his neck to be cut.

The inevitable loss of US power is a kind of Primary Trend of its own. Insecurity increases…as the costs for fake security increase (more and more of the expense pays for yesterday’s security… military pensions, legacy weapons systems maintenance, veterans’ benefits, interest on ‘defense’-inspired debt, etc.)

But the real risks to the US are neither in China, Israel or the Ukraine. They’re right at home, the usual, predictable ones – financial and political. The US is spending more than it can afford. If it continues, it invites more inflation, bankruptcy and weakness.

And with the decline in US power comes a decline in US leadership. Those with the ‘power of the purse’ can barely elect a speaker…and when they do, they choose one of the biggest dopes in the House. How can they tackle difficult trade-offs…or confront the powers-that-be behind the lurid and distracting headlines?

Joe Biden claimed, ‘American leadership is what holds the world together.’ If that were true, the world should buckle up. Fortunately, Biden’s palaver is just the blah-blah of the geriatric Caesar of a degenerate empire.

Only a small group of Republicans has shown any interest in cutting back on spending. And even they are deeply conflicted by their desire to maintain the empire at all costs. Fund the Ukraine…fund Israel…fund a new war against China! The result is: no serious cost cutting is ever considered…and no serious effort is made to ‘balance the budget.’ In fact, there is no budget to balance…just a series of ‘omnibus spending bills’…stumbling…improvising on the way to catastrophe.

The financial disaster is so clear…so obvious…and becoming so imminent…that only a fool could miss it. Yet, somehow…in one of the great mysteries of modern democracy, ‘the people’ have elected about 450 of them.

Editor's Note: Omar Ayales is the Senior Trading Strategist & Editor at GCRU (Gold Charts R Us). If you have any questions, you can reach him at oayales@adenforecast.com or visit www.goldchartsrus.net.

Hard Stuff

Gold's Seven Year Cycle

By Omar Ayales

It’s easy to lose the sight of the forest for the trees, especially when wars are breaking out, globalization is being re-defined, and inflation is running at the wildest rate in decades.

Following inflation have been interest rates globally. Moreover, the last 2 years have seen persistent rises in interest rates with an intensity not seen in decades.

But what really is at stake here?

Zooming out from current global conditions and looking at price movement over a longer-term period allows us key perspective of what to expect moving forward as it pertains to interest rates and gold. Not only next year, but quite possibly, the next 10.

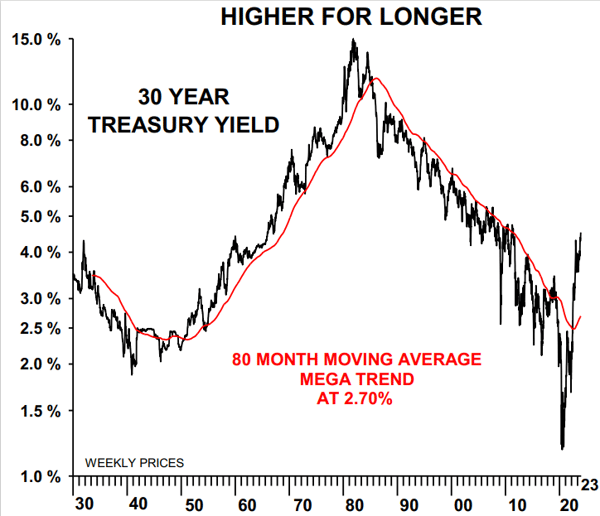

Last year in 2022, interest rates in the U.S. broke above a critical mega downtrend at the long end of a curvesince 1981. The break triggered a mega shift suggesting higher interest rates are here to stay for longer, very possibly over the next 30-40 years.

It doesn’t mean rates will rise in a linear way, over the next 30-40 years. There will be pull backs, dips and secondary reactions. But the primary trend will remain favoring higher rates for longer for many years, like the period that went from 1940-1980. Notice this first chart; a long-term chart of the U.S. 30-year treasury yield. You can see the past 2 mega trends clearly and it provides a awesome road map moving forward. It’s telling us higher for longer interest rates are here to stay.

The breakout in longer term yields, above the 40+ year mega down-trend, is a shift of systemic proportions, pushing the world into a new normal that we’re yet to discover its implications. Interestingly, it’s coinciding with a key and major intermediate 7 year low in gold. Both the ongoing rise in benchmark interest rates, together with the rise in gold suggests inflation is here to stay. And if economic activity is growing, as in the U.S., the eroding effects of inflation are not really felt. But, if economic activity stagnates or falls and inflation persists, it could lead to stagflation, and a pain reality for many where higher unemployment and higher inflation co-exist.

The above is a real possibility given the current entanglement of globalization. Consider economic strength in the U.S. contributes to global inflation of asset prices, but asset prices are not only defined by what happens in the U.S. It’s also affected by what happens in China, India, Europe, Japan, Latin America and other global economies. If the economy in the U.S. starts to cool down right as the Chinese economy starts picking up steam, for example, it could foster a situation where prices of resources and energy in the U.S. stay high even though economic activity scales back and unemployment rises.

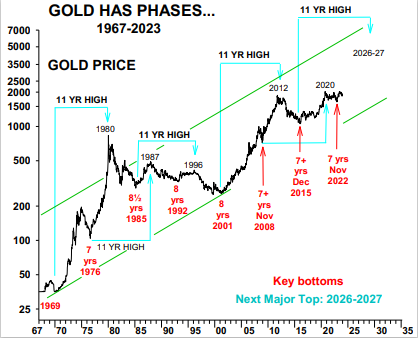

Gold’s Cycle

Consider since the early 1970s, gold has reached a mayor bottom every 7 to 8 years, 8 years during primary bear markets in gold, and 7 years during primary bull markets in gold.

You’ll notice the chart dates to just about 1970. Notice that every 7-8 years since 1970, gold has reached a critical low from which it then starts a new up move that leads to a major top some 4-5 years after, the total move (7 + 4-5 years) adds to 11 years.

This means, that every 7 year low sees the start of longer term move that ultimately reaches an 11 year high. The last 11 year peak was in 2020, the one before then in 2011, then in 2003 and so forth.

The last 7 year low was in Nov 2022, before then in Dec 2015, before then, Nov 2008, before then in 2001, and so forth…

And although past performance is not indicative of future results, it’s telling us gold’s next 11-year top is likely in 2026-7, some 3-4 years from today. The chart is saying the next major low level will be in 2029.

It’s also noteworthy that since the more recent secular bull market in gold began in the early 2000s, gold has reached a low during the month of Nov on 60% of the times.

And considering global conditions, particularly with open wars in Eastern Europe and the Middle East, the latter particularly sensitive as it can easily spill into a world war; with tensions brewing in the South China Sea, global fragmentation that is redrawing globalization and energy transformation, it seems unlikely gold, inflation or interest rates will fall into deeper bear markets or prolonged declines.

Moreover, consider that although China’s economic recovery has disappointed this year, its on an upward path, with government spending lots in ways of stimulus, working towards providing additional security for business to develop. Although much of the love from the west has faded, China will remain a key player globally, putting pressure on supply chains, keeping prices higher.

The time to buy gold is now, particularly if gold confirms a clean breakout above critical resistance at $2,000, opening the door to higher levels. For now, gold has support above $1,925, $1,815 and $1,675.

Global conditions are ripe for ongoing uncertainty turmoil and upheaval, a perfect storm that will likely continue to fuel gold up over the next few years. Be sure you buy gold during dips as well as the miners.

Editor's Note: Nomi Prins is a best-selling author, financial journalist, and former global investment banker. At Rogue Economics, Nomi shines a light on the collusion that happens between Wall Street and Big Government behind closed doors, and she provides actionable steps for readers to protect and grow their wealth. This article was originally published on October 17, 2023. Click here to discover more of Nomi's insights.

The Inside Story

Political Drama, Middle East Conflict, and Record Debt Is Fueling the De-Dollarization Flames

By Nomi Prins

As you read this, the U.S. debt smashed through a record level of $33.5 trillion. And it’s rising by the minute.

But this isn’t the only cloud on the domestic or global horizon…

As you know, last week, Hamas launched an unprecedented attack on Israel. Israel declared war on Hamas in retaliation.

And regional and global ramifications are mounting in the Middle East in a very fluid, escalating situation.

At the same time, Congress has no Speaker. The 2024 congressional budget debates continue, with no agreement on an official budget. And the war in Ukraine rages on.

With all of the turmoil, global volatility, and booming U.S. debt, one story hasn’t been getting much attention lately. But it could have an even bigger impact on your money.

I’m talking about the global push away from the dollar, which I’ve been writing about in these pages.

Today, I’ll show you how the BRICS+ bloc is angling to break the U.S. dollar’s position… And use it as more fuel for its de-dollarization fire.

The De-Dollarization Wave Is Sweeping the World

To be clear, the U.S. dollar isn’t going away.

In fact, it has been bolstered as a safe haven in the wake of the Hamas attacks on Israel… And Israel’s latest call for 1.1 million Palestinians to evacuate Gaza in what could be a pre-emptive move into ground strikes.

And, as I wrote last Thursday, the dollar won’t cease to be the world’s primary reserve currency in any of our lifetimes.

But steps are underway right now to curtail some of its uses.

That matters because its influence and power in many ways helped steer the U.S. economy over the past few decades. Now, swipes against it are growing in number and severity.

The dollar has been the world’s main reserve and international business currency since the end of World War II. That’s when the U.S. became the global economic superpower it is today.

And although it’s still on top, the U.S. dollar’s share of central bank currency reserves has dropped from more than 71% in 1999 to 59% today.

Meanwhile, the euro stands at 21% and the Japanese yen around 6% of global central bank reserves.

In the past, U.S. dollar alternatives and rivals came from other G7 currencies like the euro and even the British pound sterling.

[G7 stands for Group of Seven. It’s a political forum consisting of Canada, France, Germany, Italy, Japan, the United Kingdom, and the United States.]

These currencies largely offered stability and minimal volatile swings, and they were in relatively secure countries that investors could rely on.

In 1999, for example, I was running the analytics group as a senior managing director at Bear Stearns in London.

The big question that year was whether the euro would overtake the U.S. dollar as the world’s reserve currency… or at least take a big chunk out of it.

As we now know, that didn't happen. King dollar still shines, just a little bit less brightly.

But, while those other G7 currencies were once seen as a threat, they aren’t the reason behind the dollar’s decline today.

The Other Contenders

Since the time of the euro’s launch in 1999, China has emerged as a true global superpower.

The Chinese economy opened its doors to the world and experienced a growth boom that offers no comparison.

But around the world, we’ve rarely seen two great powers exist without mounting competition. That competition often leads to war or proxy cold wars.

That’s why, today, China is a main driver of de-dollarization.

Yes, it is true that, for now, China’s currency as a share of global reserves remains low – just under 2.5%.

But China’s drive to replace U.S. dollar-based trade with yuan-based trade has been enough to chip away at the dollar’s dominance.

Allocation to the dollar in global central bank reserve accounts is a case in point. It fell to 59% – a 25-year low – in 2020.

China’s BRICS partner, Russia, has played a part in this. Russia’s central bank now holds about a third of all of its reserves in the Chinese yuan.

And gold also plays a factor. Central bank demand for gold in 2022 shot up 152% year-over-year from 2021. Now, gold accounts for 15% of central bank reserves.

That's about 35% higher than it was five years ago when it sat at 11%. In the process, it has displaced 4% of reserves that used to be in U.S. dollars.

And another threat to the dollar is now emerging, too.

The Latest Kindling to the De-Dollarization Fire

Last month, Indonesia announced that it was creating a National Task Force for Local Currency Transactions.

Indonesia said the move was to support its ability to complete international transactions. It was also to promote the use of its local currency, the rupiah.

While that’s true, this announcement doesn’t just impact Indonesia.

You see, in May, Southeast Asian government leaders agreed to use their local currencies in regional transactions. The idea was that this could strengthen economic relationships within the whole region.

And this decision has global currency implications, especially against the dollar.

Southeast Asian regional central banks are taking steps toward de-dollarization. Indonesia’s central bank recently signed agreements with Malaysia and Thailand to use their local currencies in transactions with each other.

Indonesia inked similar local currency transaction deals with Japan and China. It’s also actively working on deals with Singapore and South Korea.

So, on the surface, Indonesia’s latest move might be the story of a country looking out for its own interests.

But it goes much deeper than that on the global stage.

Sidestepping the Dollar Is a Megatrend

Countries like India, China, Brazil, and Malaysia are all setting up trade channels using non-dollar currencies. Their leaders are increasingly forging ways to trade directly with each other in their local currencies.

For instance, China is paying for oil and other commodities from Russia in yuan instead of U.S. dollars. And it’s pushing for currency trade deals with Saudi Arabia and Brazil.

There’s a trend of cutting the U.S. dollar out of the equation. And it’s a sign of BRICS countries’ growing dependence on fellow BRICS and other emerging market powers.

From 2015 to 2022, BRICS imports from other emerging market countries grew from 30% to 34%.

Over the same period, BRICS exports to other emerging market countries grew from 28% to 32%.

These may seem like small changes. But they do show a pattern of broadening trade within the greater BRICS and emerging market bloc of countries.

If you couple this growing trade amongst the BRICS and emerging market bloc… With more of that trade done in non-U.S. dollar currencies… It marks an undeniable shift away from the dollar.

Every new deal struck between countries that once traded exclusively in dollars to trade in other currencies chips away at the global dominance of the U.S. dollar.

That’s the math of it. And it’s no small footprint, either.

The BRICS+ account for nearly half the global population and one-quarter of global GDP. And it’s gaining more economic ground.

That’s because six new countries will enter the BRICS by January 2024: Iran, Saudi Arabia, the United Arab Emirates, Argentina, Egypt, and Ethiopia.

And while the move seems unlikely, government leaders from the BRICS bloc are discussing a possible unified currency. Think of the euro but for the BRICS.

It could even take the form of a unified central bank digital currency (CBDC) or be backed by gold.

We don’t know yet what it would look like. But we do know one thing: The push to displace the dollar is happening.

And, as I wrote last week, all of this signals a weakened trend for the dollar’s use overall.

That’s why I’ve been pounding the table on gold in these pages. It’s a time-tested way to preserve your wealth even if the dollar loses more of its value as a global trading currency.

|