|

Perspective

By Rich Checkan

Tax Day in the United States has come and gone… unless you filed extensions.

For many, the stress of preparing and filing income tax forms for both federal and state returns are things of the past. Payments for taxes due are being sucked out of accounts. Refunds for overpayment are flowing into checking and savings accounts.

More importantly, by now, most of us have crunched enough numbers to know where we stand with our finances for the balance of 2023.

That means we know how much we have available to shore up our allocations to gold for wealth insurance and to silver for profit potential.

Let’s look at both of these monetary precious metals…

Gold… the Leader

After a year where everyone doubted gold’s value to a portfolio, our leader in the precious metals complex looks poised to take out resistance at $2,000 and run.

Last year, gold was flat. I heard from clients at a couple conferences recently who still doubted gold was doing anything worthwhile for their portfolios. With inflation still an issue, shouldn’t gold be running to the moon?

In a word… No.

The headline inflation everyone has been talking about for the past year is still not under control, but it is consumer price inflation and producer price inflation… which stokes further consumer price inflation.

Assets are actually deflating… and they have been falling in value (as measured in fiat currency) for the past five to six quarters. The Federal Reserve has been tightening. That has let the air out of the “Everything Bubble.”

And when asset prices are falling...

Gold does its job of preserving purchasing power by falling slower than the rest of the assets.

Last year, the gold price was flat. That was good enough to out-perform the…

- Dow Jones Industrial Average by nearly 9%

- S&P 500 by nearly 20%

- Nasdaq by more than 33%

- Bitcoin by more than 66%

That’s not bad.

However, in 2023, we are looking for a bit more out of gold. We have already tested resistance at $2,000 a few times. We have also traded within a whisker of the previous all-time high of $2,075 set in 2020.

Gold, the sound money leader, is ready for a break-out. I don’t know exactly when it will happen, but I am convinced that every failed attempt at $2,000 right now is a dip worth buying into.

Silver… for Profit

In 2022, silver slightly out-performed gold for the year. It closed on December 31st up roughly 3%.

I expect more out of silver in 2023.

You’ve heard me say this many times before. Gold leads. Silver follows initially. Then, silver out-performs… both to the downside and to the upside.

This phenomenon is the result of silver being a smaller capitalized market than gold. Once gold establishes the trend, money flows into the silver market where it has a greater relative impact.

That is starting to play out with the Gold/Silver Ratio (GSR) – the number of ounces of silver it takes to buy an ounce of gold – starting to dip below 80. This level (or higher) indicates low prices and good entry points to buy both gold and silver.

As gold and silver prices rise, and as silver starts to rise at a faster pace than gold, the GSR will start to decline.

Further good news recently surfaced for silver as well.

The Silver Institute recently released its World Silver Survey. In it, they noted that the silver supply deficits for 2021 and 2022 were enough to eliminate the silver supply surpluses of the previous eleven years.

And they expect 2023 to be another year of silver deficit production.

And there’s more…

De-dollarization and Fear

The situation for gold and silver was already quite positive. But there is even more tilting the scales in favor of precious metals.

You can bank on that!

Of course, I am referring to the failures of Silicon Valley Bank, Signature Bank, and most recently… First Republic Bank.

These bank failures have resulted in clear and present danger in the eyes of investors. Despite the assurances from the government and the big banks that are absorbing the failed banks, investors are worried that we have not seen the last of the banking crisis.

In addition, with the weaponization of the U.S. dollar internationally, both friends and enemies of the United States are looking for alternatives to the U.S. dollar and to U.S. dollar banking options.

Trade settlements outside the U.S. dollar are becoming more common, and investors are rightly concerned about an eventual loss of Reserve Currency status for the Almighty Dollar.

I do not see an alternative Reserve Currency candidate available anytime soon, but I do see that we are walking down a path that leads to that inevitable reality. We have mismanaged our currency for decades, and we have enjoyed our elevated standard of living on the backs of the rest of the world… as they buy our debt.

However, the rest of the world is starting to realize that buying our debt is a bad investment. They are shedding their U.S. dollar reserves in favor of gold.

You should too!

Become Your Own Central Bank

There is simply no better way to secure your financial future in this current economic environment than to ensure you have your wealth insurance in place.

And for those of you who are looking for profits on top of your wealth insurance, silver is on the move, and it certainly looks like most of the upside potential lies ahead.

Keep What’s Yours by purchasing gold here.

Seize tomorrow’s profits by purchasing silver here.

Call us at 800-831-0007 or send us an email.

—Rich Checkan

Editor's Note: Mark Nestmann is the founder of The Nestmann Group, a US-centric consultancy that helps mostly American clients protect your assets, preserve your wealth and safeguard your future. This article was originally published in Nestmann's Notes on April 11, 2023. You can subscribe to Nestmann's Notes or learn more about the Nestmann Group by clicking here.

Feature

Why Gold Prices Jumped Last Week

By Mark Nestmann

If you invested $100 in the S&P 500 at the beginning of 2000, you would have about $448.08 through April 10, 2023, if you reinvested all the dividends you received. That’s an impressive of 348.1%, or 6.7% per year.

That performance also substantially outpaced the Consumer Price Index (CPI) in the 21st century for an inflation-adjusted return of about 156.5% or 4.16% per year.

That’s not a bad return on investment, all things considered.

But there’s an investment that’s done even better so far this century: gold, the metal that economist John Maynard Keynes once called the “barbarous relic.”

If you invested the same $100 into gold on January 4, 2000 (the first trading day of the year), it would be worth $606.07 today. Your money would have grown more than sixfold in those 23 years, for an average return of around 8.1% annually.

Obviously, that’s a far superior return than stocks.

Gold periodically catches the eye of the chattering classes whose eyes are ordinarily glued to their smartphones watching the value of their stock portfolios increasing (or not).

And last week was such a time. In just two days, spot gold prices increased by more than $50 per ounce, peaking (temporarily) at $2,021.76 on Tuesday, April 4.

Since then, the price has fallen a bit, but is still easily within reach of its all-time high of $2,063.20. That’s a far cry from January 4, 2000, when you could buy an ounce of gold for $281.50.

Of course, a lot of things were less expensive in 2000 than they are now. You could buy a dozen eggs for under a dollar, for instance. A pound of bread cost less than a dollar, too. The average cost for a gallon of gasoline was $1.48.

Obviously, you won’t be buying a dozen eggs for anywhere close to a dollar today. Last week, I went to the grocery store and the least expensive eggs were $3.99 a dozen. And I paid $4.69 per gallon when I filled up the gas tank in my car.

We would be the first to observe that gold isn’t a productive asset in the sense that it generates wealth. This is the reason Warren Buffett, perhaps the most successful investor in history, is on record criticizing gold as an investment.

And we agree that gold isn’t a productive asset. While some gold is used for industrial purposes, the vast majority of it sits in vaults.

And the reason for that is very simple. Physical gold isn’t an asset that can simply go “poof” and disappear.

Russia’s central bank learned that the hard way last February. Within days of Russia’s invasion of Ukraine, the United States, the European Union, and other countries froze over $300 billion of its foreign currency reserves. But the 2,300 tons of gold in the vaults of Russia’s central bank remained secure.

Indeed, global central banks purchased a record amount of gold in 2022 – 1,136 tons in all, according to the World Gold Council.

But why, specifically, did gold prices increase $50 per ounce in just two days last week?

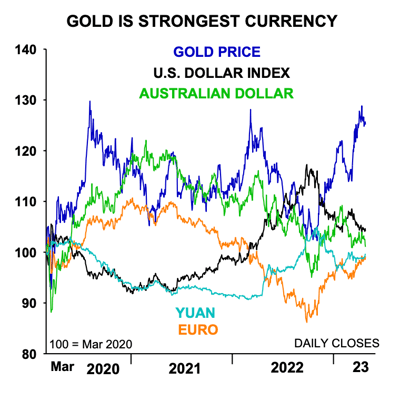

A big reason is that the US dollar’s value fell by nearly 1.5% in less than two days, as measured by the US Dollar Index, after news emerged that China and Malaysia were considering the creation of an Asian Monetary Fund to reduce reliance on the dollar.

Last week also brought news that the dollar’s share of currencies held by global central banks fell to 58.4% at the end of 2022. That’s the lowest number since 1994.

Meanwhile, yields on US Treasury bonds fell. Evidently, hedge funds and other mega-investors believe that the Federal Reserve will be forced to halt its campaign of interest rate increases.

In the 13 months, the Fed has hiked interest rates at the fastest pace in 40 years in an effort to quell inflation.

But despite the Fed’s best efforts, the Consumer Price Index inflation is still increasing at an annual rate exceeding 6%. And if the CPI were measured the same way it was 40 years ago, it would show prices increasing at around 14% annually.

At the same time, Uncle Sam is facing an imminent government shutdown, along with an ongoing banking crisis.

In such uncertain times, it’s hardly surprising that investors are turning to gold; an asset with a 5,000-year track record of protecting wealth.

Still, gold isn’t a perfect investment. As Warren Buffett points out, it’s an unproductive asset. And since it’s vulnerable to theft, it needs to be kept in a secure location, which costs money.

That’s why we’re big fans of a concept called the Permanent Portfolio, which we most recently discussed in this article.

Basically, the Permanent Portfolio consists of equal portions – 25% each – in gold, stocks, bonds, and cash.

Over the last 52 years, it’s delivered an average annual return of 8.5% and it’s remarkably done so consistently, although in 2022, its value declined by 11.6% – its worst performance in half a century. But it’s up 6.1% so far this year.

Indeed, we simply don’t know of a lower-risk long-term investment approach. When we consult with clients, we sometimes tell them to split their wealth into two imaginary piles:

1. Wealth they can afford to lose.

2. Wealth they can’t afford to lose.

For wealth you can afford to lose, feel free to invest it in whatever asset class which you feel gives you the best return commensurate with the risks you’re willing to take. But for wealth you can’t afford to lose, the best solution we’ve found is the Permanent Portfolio.

Editor's Note: Brett Eversole joined Stansberry Research in 2010. He is the lead editor and analyst for True Wealth, True Wealth Systems, True Wealth Real Estate, and DailyWealth. Brett boasts a strong background in applied mathematics and statistics, with a degree in Actuarial Science. He takes a top-down investment approach. His first goal is spotting big macro trends in the market. These are the kinds of inescapable tailwinds you want as an investor. This article was originally published in DailyWealth on April 11, 2023. Click here to subscribe.

Hard Stuff

The Gold Boom is Just Beginning

By Brett Eversole

Gold just broke above $2,000 an ounce. The metal is now just a few percent below an all-time high.

This should be big news. After all, gold was the talk of the town the first time it got close to $2,000 an ounce...

That was in 2011. You couldn't turn on the television without seeing an ad for gold... whether it was selling it to you as an investment or looking to buy your old jewelry.

Gold was in an investment boom... And everyone was on board. But today is much different.

Now, the metal is soaring – but hardly anyone cares. That's a good thing, though. It means prices can go much higher from here.

Let me explain...

Investors tend to flock to assets as prices rise. It's the most typical cycle in finance.

It begins with the bad times. Prices fall. Anyone who bought late in a boom loses big and throws in the towel. Others eventually follow suit, and sentiment washes out.

By then, the asset seems like it'll be dead money forever.

But then, prices begin to recover. No one believes it at first... But prices go up and up and up. Once the crowd sees the seemingly "easy money" stacking up, more folks return from the sidelines and push prices to new heights.

Eventually, there's no one left to buy, and prices peak once again. The inevitable decline begins... And the cycle starts anew.

That's typically the way things go. But here's the thing... Gold isn't following the playbook right now.

The metal is darn close to an all-time high. Yet investors aren't interested in owning it.

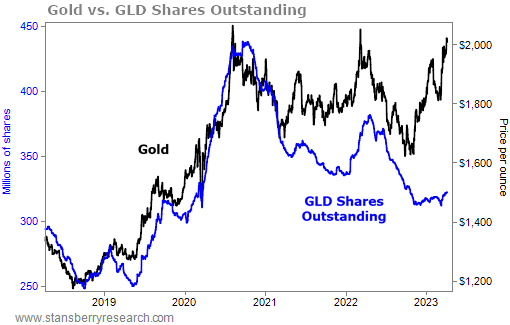

We can see it by looking at shares outstanding for SPDR Gold Shares (GLD). This is an exchange-traded fund. And that unique fund structure gives us a peek into the underlying sentiment for gold.

You see, GLD can create and liquidate shares based on investor demand. When folks love gold, and they flood into GLD to profit from it, the fund will create new shares. But when investors hate the metal and sell, GLD will lower its share count.

We'd expect to see shares outstanding near an all-time high today, given the metal's recent climb. But that isn't what's happening. Take a look...

Gold hit an all-time high and broke above $2,000 an ounce for the first time ever in 2020. Back then, investors were all over the trade. GLD's shares outstanding soared as folks poured money in.

But then, gold traded sideways. And nearly three years of dead money forced investors to move on. GLD's shares outstanding are down 26% since then.

That kind of decline made sense last fall, when gold was down a similar percentage from its 2020 high. But the metal has been on an absolute tear ever since.

It's up more than 20%... with a new all-time high in sight... but investors aren't buying.

This imbalance won't last forever.

Eventually, the age-old cycle will take hold again. Investors will notice gold's recent ascent... And they'll start buying.

That will push prices even higher. And higher prices will bring more folks in, perpetuating the cycle.

That means that even though gold is darn close to an all-time high, we haven't seen the biggest gains of this rally. This is likely the start of a multiyear boom... And that's why you need to consider owning the metal right now.

Good investing,

Brett Eversole

P.S. If you expect gold to rise, gold stocks are one of the best ways to maximize your profits. And if you want to learn more about gold and gold stocks, you should check out the Rule Symposium.

This annual event for commodities and resource investors is put on by Rick Rule, a legend in the space. You'll hear directly from mining companies and industry experts. I'll be speaking there as well this year... sharing everything I see in the metals markets, along with my favorite ways to profit.

The event is July 23-27 in Boca Raton, Florida. It's sure to be fun and informative... So if you're interested in attending, you can find the full details here.

|

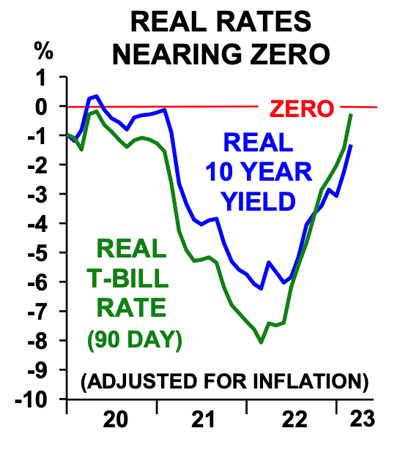

The pain of inflation can be seen with the increases in costs of things. However, until now, the labor market has been so strong that wage increases have kept up with the rate of inflation. This means the average consumer is aware of the increases in prices but does not have a problem making ends meet as they’re probably doing better off overall themselves.

The pain of inflation can be seen with the increases in costs of things. However, until now, the labor market has been so strong that wage increases have kept up with the rate of inflation. This means the average consumer is aware of the increases in prices but does not have a problem making ends meet as they’re probably doing better off overall themselves. Gold’s Perfect Storm

Gold’s Perfect Storm