|

Perspective

By Rich Checkan

September was not particularly good for gold and silver prices. And October did not start out so well either.

Earlier this week, gold prices in U.S. dollars dipped to 7-month lows. Gold dropped well below $1,850 per ounce. Silver dropped well below $21.50 per ponce.

As a result, I’d like to begin this month’s Perspective by reminding you about what I said to wrap up last month’s Perspective…

“However, I would expect central bank buying to continue given the instability of a world that is polarizing.

That should provide sufficient support to the gold price as retail investors come back into the market in this traditionally strong period from September through February.

Sprinkle in peaking bond yields, a pause in interest rate hikes, labor market weakness, wage stagnation, debt concerns (at every level), and the potential for recession and default (at various levels), and I think you have a recipe for higher gold prices.

The good news is I don’t see this happening overnight. But the trend has been building for some time. So, don’t delay further. Take care of your allocations now… for gold as wealth insurance… and for silver for profit motive.”

Of all the issues raised above, I believe debt – government, corporate, and individual – to be the most important issue of them all. It is a topic I expect to hear quite a bit about today as I am attending and speaking at The Porter and Company Annual Conference 2023 hosted by Porter Stansberry.

You can also expect to hear more about debt and the crisis it may very well trigger in the articles contributed by both Brien Lundin and Dennis Miller in today’s newsletter. Brien sums up quite well how the Federal Reserve’s current path is confusing the markets as our economy careens toward a pretty obvious and unpleasant reality.

Our good friend and honest broker, Dennis Miller, shares a very insightful interview he conducted with another good friend and Honest broker, Chuck Butler. Dennis and Chuck tell it like it is, and they identify key changes that need to be made to right the course of the United States’ economic ship.

If you like what you read today – and I cannot fathom why you would not – please do me a couple favors…

1. Subscribe to Dennis Miller’s Miller On the Money. It is a free newsletter, but Dennis relies upon free will donations from his readers to continue to research and publish his thoughts. So, please donate whatever you can to his cause as well. We need this voice of reason to continue to slap us back into reality. Your donations have the power to keep Dennis coming week after week. And… we need this now more than ever!

2. Consider joining Brian Zweig and me in New Orleans from November 1-5 for Brien Lundin’s New Orleans Investment Conference. This has been a can’t miss event for Michael, me, and Asset Strategies since Brien’s mentor, Jim Blanchard, started it in the 1970’s.

Jim Blanchard and this conference were the start of the Hard Money Movement in the United States. They are a big reason why you can own gold today to protect you and your family from the poor leadership and fiscal irresponsibility of Congress.

If you care, even remotely, about gold, responsibility, and accountability… I urge you to do your part to make sure these two fine institutions prosper well into the future.

Thank you in advance for anything you are able to do.

Speaking of Congress…

Surprise! Surprise!

Over the weekend, in a last minute, eleventh hour, stop gap measure… Congress averted a government shutdown by passing a temporary funding resolution. The resolution keeps the government operating until November 17th, 2023.

Did anyone see that coming?

Oh. That’s right. Everyone saw this coming.

If you need any further proof that Congress continues with business as usual, look no further than this last minute, and very temporary, compromise. If you need any further proof that Congress will continue to feign fiscal responsibility as it continues to spend money we don’t have, look no further than this last minute, and very temporary, compromise.

If you need any further proof that you should be buying gold with both hands at these prices… just like the world’s central banks are doing, look no further than this last minute, and very temporary, compromise.

Congress is clear. It will not change its spots.

The inevitable consequence is the continued weakening of the U.S. dollar, the continued weakening of the U.S. economy, and the continued depletion of your nest egg.

Donate to Dennis.

Join us in New Orleans.

Buy gold and silver at these oversold prices.

Then… sleep well at night as you Keep What’s Yours!

Call us at 800-831-0007 or send us an email today so we can help you get your precious metals allocation in order.

—Rich Checkan

Editor's Note: This article originally appeared on September 28, 2023 in Miller on the Money. Miller on the Money is a FREE weekly publication which we highly recommend. We suggest you sign up HERE.

Feature

What Happens When The World No Longer Wants, Or Needs U.S. Dollars?

By Dennis Miller

Chuck Butler and I recently discussed how government deficit spending, and monetizing the debt has caused a worldwide awakening. Inflation is killing the value of the dollar, and our creditors understand that.

But wait, there’s more! The interview continues….

DENNIS: BRICS used to stand for Brazil, Russia, India, China and South Africa. Global Research reports, Doomsday for the Buck? A Reserve Currency Is No Longer Needed. DENNIS: BRICS used to stand for Brazil, Russia, India, China and South Africa. Global Research reports, Doomsday for the Buck? A Reserve Currency Is No Longer Needed.

Quoting Paul Craig Roberts:

“It was Washington’s economic sanctions against Russia, the theft of Russia’s central bank reserves, and the theft of Venezuela’s gold, not the conflict in Ukraine, that weaponized the US dollar and resulted in global realignment.

…. The US dollar is used as world money to settle imbalances in international trade, but the sanctions woke the world up to the risks of using the dollar.

Consequently, the BRICS suddenly expanded, (adding) Argentina, Egypt, Iran, Saudi Arabia, and the United Arab Emirates. The organization now contains essentially the entirety of world oil production and 40-45% of World GDP.

…. Saudi Arabia announced the end of the petrodollar when it began accepting payment for oil in other currencies. The BRICS are working out how to carry on trade among themselves without use of the US dollar, which in effect brings to an end the role of the dollar as world reserve currency.

…. What this means…is that the US will begin having financing problems for its large budget and trade deficits. As long as the dollar was the world money, foreign central banks kept their reserves in US Treasury debt.

…. The situation is changing. If…about half of the world’s population and 40-45% of world GDP cease using the dollar, the foreign central bank market for US debt shrinks considerably. Having offshored its manufacturing, the US is import-dependent.

Declining use of the dollar means a declining supply of customers for US debt, which means pressure on the dollar’s exchange value and the prospect of rising inflation from rising prices of imports.”

RT adds fuel to the fire:

“In terms of oil reserves, BRICS will also control nearly half of the world’s total, 719.5 billion barrels out of 1.6 trillion. If Venezuela, which has recently applied for membership, is accepted into its ranks, the group’s control will be even greater – around 65.4%. In comparison, the G7 group …. (The US, UK, Germany, Italy, Canada, France, and Japan) controls only 3.9% of known crude reserves.”

This is overwhelming; let’s break it down.

Chuck, Nixon cut a deal with the Saudis creating the petrodollar, solidifying the USD as the world currency. Because the US weaponized the dollar, aren’t the BRICS really uniting to reverse the process?

If so, why does the world need dollars?

CHUCK: Well, that’s the point, isn’t it Dennis? Even Gomer Pyle shouldn’t be surprised. It should have been expected.

When the Saudis removed the USD requirement for oil contracts, the game was over. No longer THE PETROL DOLLAR, is the death knell.

Weaponizing the U.S. dollar doesn’t’ mean adding guns to it; shutting Russia out of SWIFT, and freezing their dollar assets in the U.S., was considered to be weaponizing the dollar.

The world saw this and said, “if the U.S. can do this to a country like Russia, they sure as hell can do it to us”. “Weaponizing” the dollar through exclusion of the SWIFT payment system forces other nations to seek other alternatives to trade freely in the world market. They must protect their citizens and be able to sell their exports in order to survive. Our government’s actions really accelerated the demise of the dollar as the world currency.

They began reducing their dollar reserves and buying Gold. Central Banks around the world bought 1,136 Tons of Gold in 2022; a record for a year’s worth of buying! Can’t say I blame them either…

Once countries realize they have no need for dollars in reserve; there goes the neighborhood!

DENNIS: Let’s look at consequences of these acts and how it affects all of us. What do you expect?

CHUCK: Throughout history, several countries enjoyed the esteemed reserve currency status and lost it by ignoring the responsibilities that it entails.

Spain, the Dutch, England, and others once had the privilege of their currency holding the esteemed “reserve currency” status. When they lost that status, their standard of living, their way of life, changed dramatically – for the worse!

Their fate will be our fate… When a country loses the reserve status everything becomes more expensive. When the Beatles came to the Ed Sullivan Show in the early 60’s, they showed pictures of Liverpool England to give us an idea of where the boys came from. It was depressing, looking like a country in near ruins.

My favorite example was how U.S. gas prices were much cheaper than in the U.K. That will go away; particularly when you look at the BRICS nations and their control over energy supply. Higher gas prices affect everything we buy.

This is just an example, but NOT an isolated example; everything we import into the U.S. will be much more expensive than it is today – by a large margin.

People are finally understanding what I preached for years; the U.S. was sending all of its manufacturing overseas. Remember Ross Perot saying, “The giant sucking sound,” referring to jobs leaving our country? If the jobs hadn’t gone elsewhere, we would not be subjected to mass price increases… I’m just saying…

DENNIS: Doesn’t this create a dilemma for much of the world? If they all started dumping their trillions in US debt, it would cause the dollar to collapse and they would lose trillions. How do you see this panning out?

CHUCK: Yes, it would. I’ve warned that Treasuries were in trouble. I envisioned all the countries of the world sitting around a conference table in a room with one door. Should they all run for the exit at the same time, the doorway would become jammed up, and the trading would be very nasty.

J. Paul Getty said, “If you owe the bank $100 that’s your problem. If you owe the bank $100 million, that’s the bank’s problem.”

The big boys get it, and will work together to do a calm, zipper-like exit so things go smoothly. This is what the creation of the BRICS will do. They will coordinate their selling so that it doesn’t upset the apple cart of dollar and Treasury trading.

DENNIS: It sounds like musical chairs, they want to get rid of their debt holdings, let some other poor sucker be holding the bag when the music stops; then boom!

I’m concerned, the government is still spending and borrowing at historic levels. Not only will they need to finance their current deficit spending, but they also must roll over existing debt as it matures.

Bonner says it is “inflate or die!” If interest rates rise in a free market, could it literally bankrupt our government and cause us to default?

CHUCK: Absolutely! I’ve subscribed to the “inflate or die” saying, and believe that’s what the leaders of this country have to decide; which road they will take, high inflation or massive tax increases and spending cuts.

No matter which one they choose, both roads lead to misery… One just gets you there faster…

Treasury yields will continue to rise; that’s the only way the U.S. can make them attractive to buy. Eventually, without massive spending cuts and higher taxes, the U.S. will have to buy its own bonds, monetize the debt, creating even higher inflation. That’s a mess that will really shove down any remaining credibility of the U.S. government and dollar.

The higher interest cost to service the bonds will cut into the tax collections that help support this country. Bond servicing costs have already passed the cost of national defense. Next is Social Security and Medicare… Then… default… The higher interest cost to service the bonds will cut into the tax collections that help support this country. Bond servicing costs have already passed the cost of national defense. Next is Social Security and Medicare… Then… default…

DENNIS: While default sounds simple, I see terrible implications. You’ve said the politicians must STOP SPENDING money we don’t have – immediately. They won’t do that willingly; with understandable fear the welfare class will storm the palace.

Since the Tea Party movement, the public has been trying to push back; yet the entire political class ignores it, referring to it as voter “hissy fit.” Both parties continue to govern against the will of the majority.

While things can’t go on as they are forever, is true political reform a possibility without a real overhaul in our political system?

CHUCK: Let’s go back to “inflate or die.” Sometimes it takes a true crisis, not a made-up political one, to get politicians off their butts working together. They face some tough choices.

| Politicians become motivated when they see it is in THEIR best interests to do what is right. |

Remember when citizens stormed the Fed when Volcker raised interest rates? Well, they are likely to do the same if/when inflation skyrockets. Historically, a revolution results; sometimes just taking place at the ballot box. Let’s hope that is what it takes.

I think most citizens will be willing to sacrifice some if they see true reform, not just Congress looking after special interests….

Editor's Note: Brien Lundin is the Publisher of Gold Newsletter and CEO of the New Orleans Investment Conference. It's not to late to join Brien, Rich, and many many more at the New Orleans Investment Conference on November 1-4, 2023. Register today!

Hard Stuff

Hopes on Hold

By Brien Lundin

Markets tremble — and gold weakens — as investors finally start taking the Fed seriously and the U.S. economy refuses to collapse.

Still, with a global economy built upon a foundation of zeroed interest rates being pummeled by one of the harshest tightening cycles ever seen, everyone seems to be simply waiting for whatever will spark the next crisis.

While the headline above sums up the views of gold bugs, for just about every other investor right now, something along the lines of “Fearing The Future” would be more appropriate.

You can sense it in the air — the feeling that something looms just ahead.

You don’t have to look hard to see it in the comments and mannerisms of the talking heads on CNBC, as they strain to explain why repeated stock sell-offs are nothing to worry about. Yet their own headlines and chyrons, like “stocks close down for fourth straight day” tell a different story.

There are lots of cross-currents in the financial and macro-economic world today, but I think we can peer through the fog and distill it all down to this: After well over a decade of the easiest monetary policy in human history, followed immediately by one of the steepest tightening cycles ever seen, we fully expect a major event of some sort that will force the Fed to pivot.

Yet Fed Chairman Jerome Powell and his minions seem blithely unconcerned about what may lie ahead, and hell-bent to maintain this ultra-hawkish monetary stance as long as possible.

The result of this tension is that investors keep trying to price in a Fed pivot, only to be forced to retreat as the Fed maintains its harsh policy and rhetoric.

Note that we get these periodic rebounds in stocks, bonds and gold even though investors have no idea where the next crisis will originate.

That said, there is no lack of potential candidates. They include the recession that every indicator continues to point toward...a stock market crash (which looks increasingly likely given the performances of the past few trading sessions)...the always-concerning derivative-market dominoes...the soaring cost of servicing the federal debt (which will make headlines next month as official numbers put it well past $1 trillion annually)...and the tsunami of debt resets that’s about to crash on companies around the world in the weeks ahead (James Grant puts the total increased costs at $8 trillion!).

So yes, there are plenty of options and, again, it’s likely that the eventual catalyst will be something out of left field that we haven’t thought about much at all. That’s just the way the world works.

And while we are forced to wonder what will cause the next crisis, we have certainty as to what the Fed will do about it: They’ll unleash a flood of liquidity that will make the post-Covid rescue operation pale in comparison. Because, again, the addicted financial markets and economy will require a much greater dose of monetary adrenaline to get the same effect as before.

The Fed will strive for shock and awe, and you can bet that they’ll get it.

But we know all this. The real question isn’t so much what will happen, but when. And that’s the tough part, as it usually is.

So far, any bet that the inevitable crisis is imminent hasn’t turned out well. We’ve seen a few short-lived rallies in stocks, bonds and gold this year, and they’ve all come up short as the Fed has renewed its vow to bury inflationary pressures for good.

I must admit that I’m very impressed with Jerome Powell’s fortitude. My friend Danielle DiMartino Booth, who is probably today’s top Fed analyst (as well as a speaker in New Orleans this year), has told me that she believes Powell idolizes Paul Volcker and wants his legacy to be mentioned in the same breath as his famed predecessor.

The problem is that Powell doesn’t have the same toolbox that Volcker had at his disposal. When Volcker was hiking rates to over 20%, the federal debt was merely 35% of U.S. GDP; today it’s about 125%.

We simply cannot afford to pay the costs of servicing this massive (and rapidly growing) debt load with anything approaching normalized interest rates.

In light of this simple math, and the markets’ addiction to ever-easier money, I never would have expected Powell to turn the Fed’s outspoken doves into such ardent hawks and to show such resolve in raising rates no matter what the consequences.

That said, the consequences will come...and they’ll have to deal with them when they do.

The Turning Point Is Near

With the Fed expressing its determination to keep rates higher for longer...and with yields soaring as the Treasury issues a flood of new paper to fund ballooning deficit spending...the economy and markets are headed for a showdown.

The turning point will be dramatic and likely not too much further in the future. You need to know what’s likely to happen, and how to protect yourself and profit.

One of the best ways to learn how to do so is by attending the upcoming New Orleans ’23 Investment Conference, featuring one of the greatest rosters of experts ever assembled.

Consider who you can hear from in just a few weeks:

Matt Taibbi...James Rickards...Danielle DiMartino Booth...George Gammon...Konstantin Kisin...Rick Rule...Dominic Frisby...Brent Johnson...Lyn Alden...Rich Checkan...Dave Collum...Peter Boockvar...James Stack...Peter Schiff...Jim Iuorio...Tavi Costa...Adrian Day...Adam Taggart...The Real Estate Guys...Gwen Preston...Brent Cook...Mark Skousen...Nick Hodge...Robert Prechter ...Chris Powell...Economic Ninja...Albert Lu...Gary Alexander...Dana Samuelson...Jeff Hirsch...Steve Hochberg...Mary Anne & Pamela Aden...Bill Murphy...Gerardo Del Real...Omar Ayales...Keith Weiner...and more.

And, of course, yours truly. I always save my best forecasts and recommendations for this legendary event...and I can guarantee that you won’t want to miss my special presentation for this year.

Again, it all happens in just a few weeks — from November 1-4. So CLICK HERE (or call us toll free at 800-648-8411) to secure your place now...guarantee accommodations in our host hotel...and save up to $400.

Editor's Note: Frank Holmes is the CEO of U.S. Global Investors —a company that produces quality analysis concerning gold, precious metals, natural resources, and emerging markets—in conjunction with his work as a fund manager. Frank is a long-time friend of ours, and we've chosen to share his article originally published September 28, 2023. For more articles like this from Frank and other leading experts, you can subscribe to the U.S. Global Investors newsletter here.

The Inside Story

Short-Term Treasury And Municipal Bond Funds In A High-Interest Rate Environment

By Frank Holmes

With interest rates at multiyear highs, it may be appropriate right now for investors to consider investing in U.S. Treasuries and municipal bonds with shorter maturities between one and five years. Historically, such bonds have been less sensitive to the vagaries of the Federal Reserve and its aggressive rate-hiking scheme.

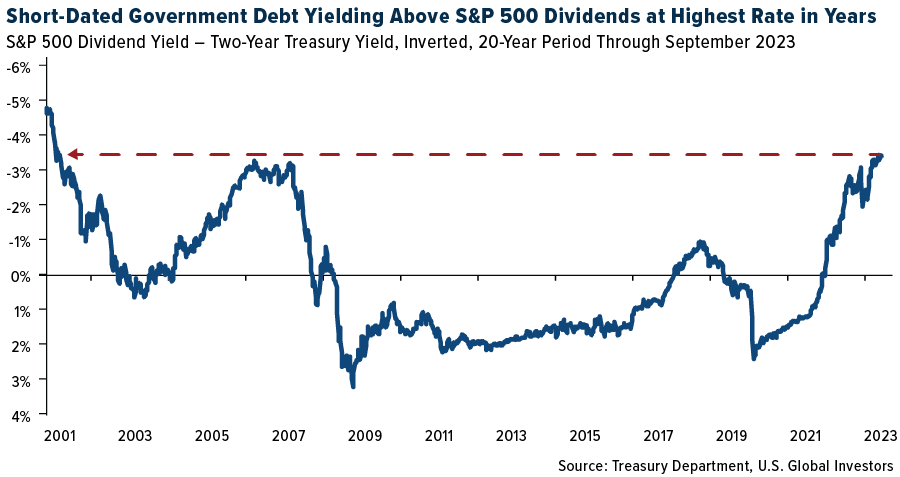

The Fed’s hawkish approach has kept short-end yields high, with the yield on the two-year Treasury surpassing that of the 10-year bond by about half a percentage point, signaling an inverted curve and deterring investors from less liquid, longer-term bonds.

Currently above 5%, the two-year yield is even significantly above the S&P 500’s dividend yield of around 1.6%—the greatest such difference in over 20 years.

Is Consumer Spending Overestimated?

Despite three consecutive favorable inflation reports, the Fed’s guidance shows an expectation to maintain a higher key rate through 2024, with a possible rate hike later this year due to the economy’s surprising resilience. The Treasury Department’s accelerated pace of debt issuance, highlighted by a net raise of $1 trillion through bond sales in the third quarter, is further pressuring the bond market.

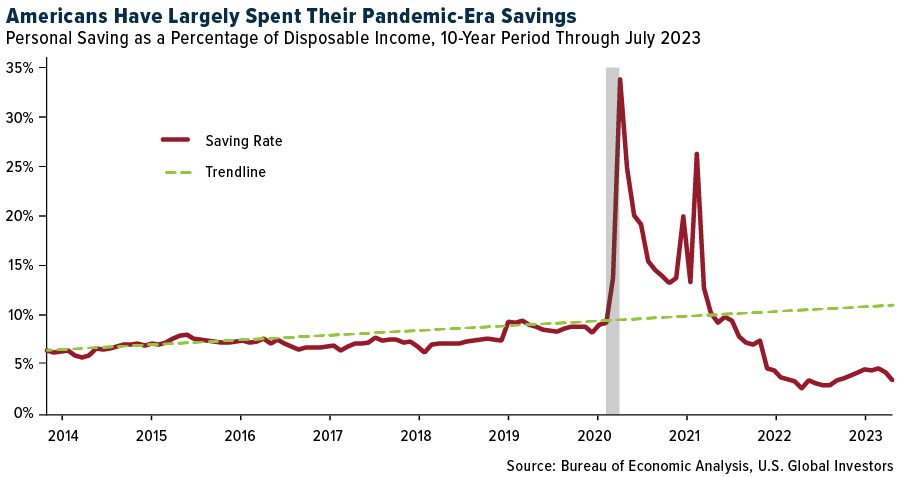

However, I believe that the strength of the U.S. consumer, cited by Fed chair Jerome Powell as the key reason for believing that high rates will only modestly slow down growth, is overestimated. As you can see below, the extensive savings accumulated by households during the early months of the pandemic, which protected the economy against back-to-back rate hikes and an inflationary shock, have been largely spent.

The Quest For Higher Yields

Municipal bonds—debt issued by state and local governments—are likewise yielding more than they have in years, but many investors are flocking to money-market funds and high-yield savings accounts, some of which are offering returns as high as 5.5%, compared to the 3% to 4% yield from the best-rated AAA municipal bonds.

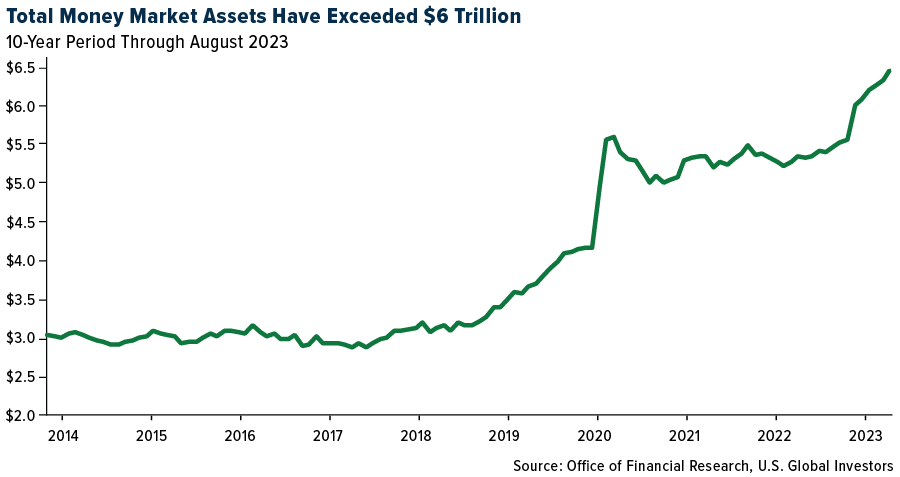

Despite the fact that munis offer income that’s tax-exempt at the federal and often state and local levels, the higher yields in alternative investments continue to divert investors who may be wary of interest-rate risks—even at the cost of potentially missing out on a bond market rally if economic conditions shift and the Fed cuts rates in response. This year, money market funds have attracted some $870 billion in fund flows this year, pushing total assets above a head-spinning $6 trillion for the first time ever.

This shift in preference, driven by the allure of higher yields, has deterred investment in munis—traditional safe havens with tax-free interest benefits. Muni mutual funds, pivotal buyers of state and local debt, have witnessed a stark withdrawal of around $6.2 billion in 2023, contributing to a challenging scenario for boosting performance in the $4 trillion muni-bond market.

NEARX And UGSDX

The selloff in short-term Treasuries and muni bonds, I believe, makes them even more attractive as portfolio diversifiers and potential hedges against equity weakness. As billionaire investor Warren Buffett once said, it’s wise for investors to be fearful when others are greedy and to be greedy only when others are fearful.

We’re pleased to offer two fund options for investors seeking exposure to short-dated government debt.

Near-Term Tax Free Fund (NEARX)

NEARX is focused on investing in municipal bonds that have a relatively short maturity, aiming to offer tax-free monthly income at the federal level and often state and local levels. Under typical market conditions, a minimum of 80% of its net assets are invested in investment-grade municipal securities, which are free from federal income tax, including the federal alternative minimum tax.

Just under 40% of the fund is invested in munis with a maturity of under one year, while approximately 60% is between one and five years.

U.S. Government Securities And Ultra-Short Bond Fund (UGSDX)

UGSDX is designed to invest in U.S. government bonds and obligations while aiming for a higher level of current income compared to what money market funds provide. UGSDX caters to investors who’re interested in capital preservation while earning a potentially higher level of income.

Roughly 87% of the fund is invested in bonds with a maturity of under a year.

|