|

Perspective

By Rich Checkan

Welcome to the dog days of summer!

A month has passed since I last wrote to you… but very little has changed…

• The U.S. dollar is still under pressure. It trades below $100 on the U.S. Dollar Index… down 10% on the year.

• U.S. equities continue to trade at dizzying heights with valuations similar to 1929 and 1999. What could go wrong from here?

• Central banks continue to buy gold as if it were going out of style.

• Gold continues to be a steal at prices just below all-time highs.

• Silver continues to be an even better steal at prices at just 60% of all-time highs.

• Western investors continue to sit on the sidelines trying to make sense of gold and silver prices.

• I continue to scratch my head… wondering how they do not see what I see very clearly.

But there is something new this month.

The U.S. debt no longer sits at $36 trillion and change. The U.S. government now owes over $37 trillion in debt!

Not Surprising

For those of us paying attention, it should not be a surprise that we breached $37 trillion. Nor should it be surprising how little time it took to reach $37 trillion after we reached $36 trillion.

What we are doing as a nation comes right out of the crumbling empire playbook.

We overextend our reach, and the empire becomes too far-flung to maintain.

We over promise to secure votes, and the empire cannot afford to pay for all it promised to deliver.

We overestimate our political clout, and less and less of the world appreciates our role.

We over supply the world with our currency, and each and every currency unit in circulation is “worth less” than it was the day before.

The late, great Paul Harvey famously said…

“When your outgo exceeds your income, the upshot may be your downfall.”

I have also heard it quoted as “your upkeep” as opposed to “the upshot.” But you get the idea.

Why is it that our politicians have not been able to figure this out?

President Trump and Congress Could Fix This Mess

It would be simple.

Congress just needs to make sure they pass no spending bills that are not balanced. If there is not enough revenue to cover expenditures, the spending bill should never be passed.

If the spending bill is so critical that it must be passed… and the money must be spent… find spending elsewhere that can be cut to make room for the new critical spending.

And President Trump… and anyone who follows him… should never sign a spending bill that is not balanced.

Again… remarkably simple.

Of course, the difficult part in all this is that they will not be re-elected if they do not deliver on the promises that convinced voters to elect them in the first place.

This is the issue. Politicians want job security. Therefore, they must deliver on the promises they made… whether there is money in the budget or not.

Newsflash… There is no money in the budget. That well ran dry roughly $37 trillion ago.

Inflate or Die

As a result, we are reminded of the words of the venerable Bill Bonner… “Inflate or Die.”

That is where we find ourselves. The Treasury will continue to expand the money supply… creating new dollars out of thin air… to paper over the sins of Congress and the President.

In the end, everything of any value will cost more in the future. It will take more “worth less” dollars to buy them.

Gold has a clear value. Silver does too.

Both will be higher in the future. Therefore, both can be purchased more cost-effectively now. Yesterday was the best day to buy gold and silver. Today is the next best day.

There is no better way to Keep What’s Yours!

Send us an email

or call us toll free today at (800) 831-0007.

We can help you take steps today to secure your financial future for you and your family.

—Rich Checkan

Editor's Note: Nomi Prins is a best-selling author, financial journalist, and former global investment banker. Prinsights Pulse is a new, free publication that’s curated by Nomi Prins. Designed for everyone from executives at large institutions to individuals seeking to enhance their financial understanding, this powerful newsletter provides essential insights into economic trends that affect us all. This article was originally published on July 31, 2025. Click here to discover more of Nomi's insights.

Feature

The Copper Play Fueling a Global Power Shift

By Nomi Prins

Here’s a key recommendation in copper that sits at the center of the geopolitical transformation.

“Copper has been, and will continue to be, the fundamental metal of the electrical industry.”

— Sir Walter R. G. Baker, Electrical World magazine, 1920

Copper is one of the first metals used by humans 11,000 years ago. It is the second most conductive metal on the planet and has played a crucial role in history, ranging from early weaponry to coins to electricity. Now, electricity, like copper, is entering an exponential use period as the world’s insatiable demand for power is on a seemingly unstoppable path.

History shows us that when the need for certain assets booms, the desire to control them grows even more. That’s why August 1 will be a key transformational day for copper. That’s when a crucial 50% U.S import duty on copper is set to take effect. And, even if trade agreements surrounding that line in the sand don’t fully transpire, the proposed tariff itself means the stage has been set for more scrutiny over copper supply chains for months and years to come.

The change is important to monitor because the White House trade measure covers cathode, wire rod, and semi-finished copper products. These aspects cover nearly everything that U.S. manufacturers rely on to power factories, build grids and run electric vehicles.

This trade policy represents the realization that copper, both raw and refined, is strategically important to energy and national security. The historic maneuver also creates a tangled, fragmented trade environment that is as much geopolitical as it is economic.

Across the planet, governments, businesses and traders have been scrambling to adjust and understand the broader implications of this action. This rapid movement recently pushed copper to record highs. It has also pressed key multinational copper companies to up their bid for global market share – with one in particular in a prime position to reap the benefits.

While the initial reaction to the White House announcement on July 30, which included copper as well as certain copper products, prompted a sharp decline in prices, we think this is an overreaction. Ultimately, copper is a long-term opportunity – and one we remain optimistic on.

What Triggered the Recent Copper Rush

On July 7, the White House formally announced a 50% copper tariff. In response, COMEX copper futures surged over 13% the next day, hitting an all-time high above $5.65 per pound ($12,330/ton). That was the largest single-day move since 1968.

Copper futures had risen steadily since to a new record of $5.79 per pound. The jump doesn’t just reflect speculative trading. It’s the market pricing in guaranteed delivery and hedging tariff risk. Even in the face of recent news with COMEX, the high demand and data tell us the real story.

Increases in copper inventory data showed a potent copper squeeze. Refined copper imports are surging. COMEX warehouse reserve levels in the U.S. ballooned to nearly 248,000 metric tons in late July. That’s more than double the March levels.

However, this physical inventory bump is misleading as a measure of demand. That’s because mostly, it’s allocated to forward-booked supply and does not represent excess capacity. That means the inventory is locked in by buyers securing supply before the tariff deadline.

At the London Metal Exchange, warehouse inventories have plummeted by about 80% this year.

This divergence between bulk buyers in the U.S. and dropping inventories in the rest of the world paints a dramatic picture. It shows that refined copper is physically moving into tariff-protected U.S. warehouses, which is draining global inventories – and pressuring prices. And that spells upside for miners extracting or producing high-quality raw and refined copper.

We Signaled This Copper Shift Last Year

The U.S. and global copper supply chain participants had been bracing for this moment for months. Last year, we discussed factors driving increasing copper demand and how it would lead to higher copper prices. Since then, the stakes have been driven even higher.

On March 3, the U.S. Commerce Department launched its Section 232 investigation into copper imports. That was the initial sign of official intent to examine the strategic importance of copper as a national defense item.

What you should know is that Section 232 is part of the Cold War era 1962 Trade Expansions Act. The act was designed to determine whether certain materials or products are critical to U.S. national security.

That’s why, the report, released on July 30, from the White House is worth paying attention to. It found that, “copper is being imported into the United States in such quantities and under such circumstances as to threaten to impair the national security of the United States.” Below, is one area of key findings that the government report detailed, noting:

“Copper is the second most widely used material by the Department of Defense and is a necessary input in a range of defense systems, including aircraft, ground vehicles, ships, submarines, missiles, and ammunition. Copper also plays a central role in the broader United States industrial base. The metal’s exceptional electrical conductivity and durability also make it indispensable to critical infrastructure sectors that support the American economy, national security, and public health. Alternatives to copper are insufficient substitutes for these vital industries and products in many circumstances.”

The 232 investigations into copper serve as a key milestone in White House efforts to secure more of the copper supply chain – and why, from raw material to refined products, they are critical.

Join Prinsights Premium to get the rest of Nomi's insights on copper and more.

Editor's Note: Frank Holmes is the CEO of U.S. Global Investors —a company that produces quality analysis concerning gold, precious metals, natural resources, and emerging markets—in conjunction with his work as a fund manager. Frank is a long-time friend of ours, and we've chosen to share his article originally published June 20, 2025. For more articles like this from Frank and other leading experts, you can subscribe to the U.S. Global Investors newsletter here.

Hard Stuff

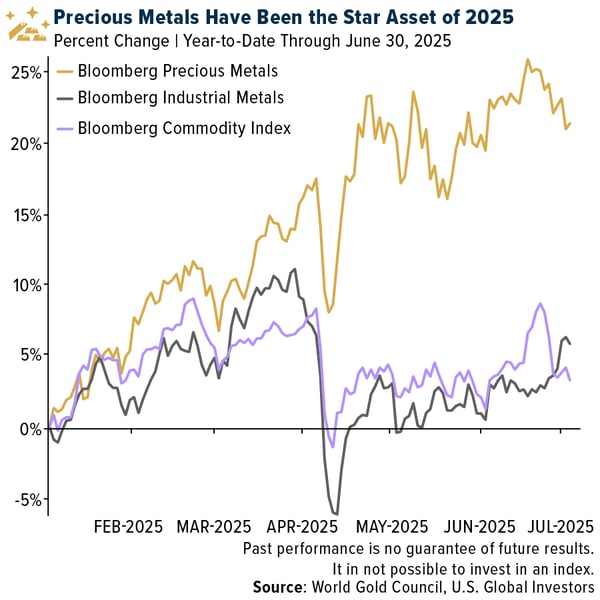

Precious Metals Crushed Their Commodities Peers in the First Half of 2025

By Frank Holmes

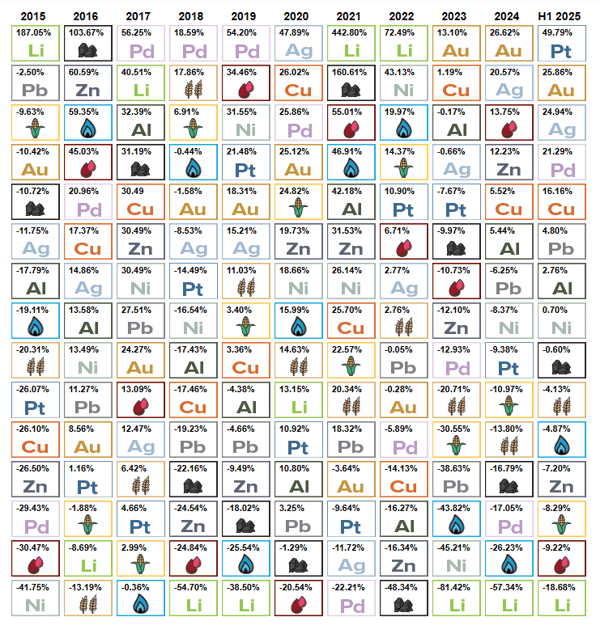

Every year around this time, we update our Periodic Table of Commodities Returns to reflect the performance of raw materials in the first six months. I’m biased, but few tools do a better job of providing a clear, interactive picture of the commodities landscape than ours.

Platinum Has Been the Year’s Breakout Star

After years of range-bound trading, platinum finally broke out in spectacular fashion. The metal surged from just over $900 an ounce in January to around $1,360 by the end of June, representing a 49.8% gain. In Q2 alone, it jumped 35.8%, closing the quarter at a price not seen since 2014.

A major factor for the spike was constrained supply. Platinum supply has historically been price inelastic in the short term, according to the World Platinum Investment Council (WPIC). Even as prices surged, production remained sluggish, leading to persistent market imbalances. At the same time, demand remained firm, spanning industrial applications, jewelry and its emerging role in green hydrogen technologies.

Unlike its cousin palladium, which is heavily reliant on gasoline vehicle manufacturing, platinum benefits from a broader range of demand. It’s used in diesel catalytic converters, fuel cells and more. And as the world moves toward decarbonization, platinum’s future in hydrogen energy systems makes it increasingly strategic.

Gold: Still the Ultimate Safe Haven

Gold has always been a barometer of uncertainty, and in 2025, investors had plenty to be uncertain about.

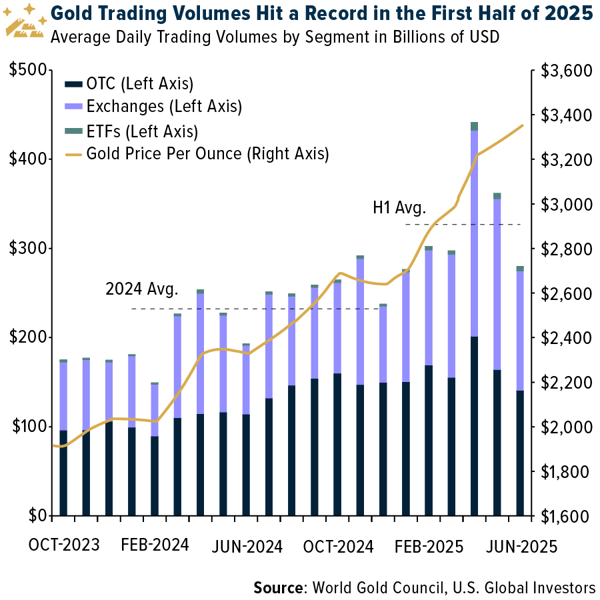

Geopolitical tensions flared again in the Middle East, with the Israel–Iran conflict intensifying. In April alone, gold hit five separate all-time highs. By the end of June, it had risen 25.9%, topping $3,300 per ounce. With central banks continuing to buy record amounts of bullion, especially in emerging markets, I believe the metal remains a clear beneficiary of macro concerns.

Physically backed gold ETFs attracted a stunning $38 billion in inflows during the first half of the year, marking the strongest performance since the pandemic-fueled rally of H1 2020. North American investors led the charge, adding $21 billion. Trading volumes surged across the board, averaging $329 billion a day globally—a new record, according to the World Gold Council (WGC).

There’s another trend at work: de-dollarization. Since the U.S. and its allies froze Russian central bank assets in 2022, many nations have grown increasingly wary of holding dollar-denominated reserves.

Gold, by contrast, is seen as politically neutral, and central banks have responded by diversifying into the yellow metal at an unprecedented pace. In fact, institutions bought more in the last four years than in the previous two decades combined.

Silver’s Dual Role as a Precious and Industrial Metal

Silver’s story is a little different, but no less compelling.

It often rides gold’s coattails, and in 2025, it’s kept pace with the yellow metal, rising nearly 25% through June. Silver briefly surged above $37 in mid-June, levels not seen since 2011, before settling around $36.

The white metal stands to benefit from its dual role as both a precious and industrial metal. Demand is rising in green energy applications, particularly solar panels and battery storage. As central bank gold demand continues to outpace silver, I believe silver is undervalued on a relative basis. A return to the historical gold-silver ratio (around 80) could send silver back toward its all-time high of $50 an ounce.

Copper: The Metal of the Future

Though not a precious metal, copper deserves an honorable mention. It finished the first half of the year up 16.2%, making it the best-performing base metal.

What’s driving copper’s rally? A perfect storm of supply fears, strong demand from artificial intelligence (AI) and data centers, and political noise from Washington.

President Donald Trump’s surprise announcement of a 50% tariff on imported copper this month sent U.S. copper futures to record highs, adding fresh volatility to an already tight market. And with global supply struggling to keep pace with demand, copper’s long-term fundamentals look incredibly strong.

Data centers alone are projected to require 127,000 megawatts (MW) of power by 2029, up from 82,000 this year. Each megawatt of capacity needs about 27 metric tons of copper. That’s not even counting the metal’s vital role in electric vehicles (EVs), grid modernization and semiconductors.

Energy and Agriculture Were the Laggards

Not all commodities shared in the rally. Several energy and agricultural materials ended the first half in the red.

Even lithium, once the darling of the EV boom, fell nearly 19%—a reflection of softening battery demand and oversupply from key producers in China and South America.

For contrarian investors, this could be an area to watch for opportunities in the second half of the year.

Periodic Table of Commodities Returns

The first half of 2025 reminds us why commodities deserve a strategic place in a well-diversified portfolio.

Precious metals have proven their worth once again as reliable hedges against inflation and geopolitical concerns. Central banks and fiscal imbalances continue to support long-term demand, especially for gold and platinum.

Industrial metals like copper are benefiting from secular shifts in technology and electrification. While energy and agriculture struggled, those sectors may offer attractive entry points for investors with a longer time horizon.

As always, our interactive Periodic Table of Commodities Returns makes it easy to compare commodity performance across years and sectors.

Editor's Note: Bill Bonner is the Founder of Bonner Private Research and owner of the Agora Companies. This article was originally published by Bonner Private Research on July 29, 2025. You can subscribe to Bonner Private Research here.

The Inside Story

Something for Nothing

By Bill Bonner and Dan Denning

The value of a pick-up truck doesn’t go down when you start the engine. ‘Ghost wealth,’ on the other hand, drives away on its own.

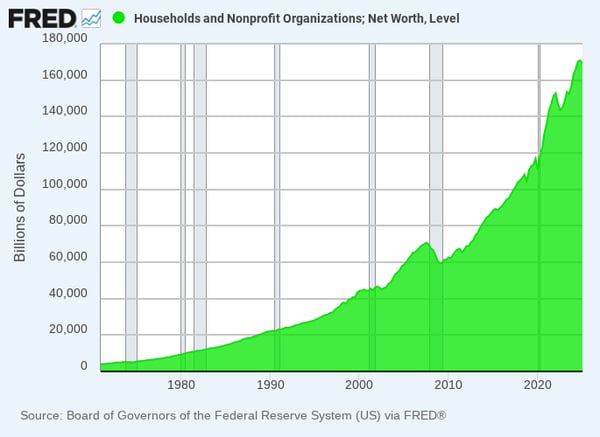

US household net worth is up nearly $60 trillion in just over five years, according to data from the Fed. Nearly half that increase is due to the rise stocks.

On CNBC, an analyst, Anthony Pompliano, told listeners that bitcoin is becoming a major source of revenue for Wall Street. People can’t wait to get into the bitcoin boom. Wall Street is developing more and more bitcoin-flavored products for them to buy.

“Over the last five years, the US dollar has lost 30% of its value,” he explained. “And the S&P, denominated in bitcoin, is down 85% since 2020. Bitcoin is a much better store of value.”

Say what? A store of value whose price goes up like a rocket? What kind of store is that? Bitcoin is trading like the biggest speculative asset since tulip bulbs, not like a safe place to store your wealth.

But let’s begin with the most basic question. Why…how…do sane, sensible people…people who put on their pants one leg at a time…trade their houses and cars for something that is as close to nothing as you can get?

And why…how…comes it to be that you can now get more than three times as many houses as you could last year…for the same amount of nothing? Twelve months ago, you would have needed about nine bitcoins to buy a house. Today, you only need three of them.

But wait. ‘Bitcoin is not nothing,’ you say? ‘It’s important information. It tells you how much money you have. And it protects your wealth from inflation.’

Maybe. But last week, we wondered how much of the stock market is ‘ghost wealth?’ A companion question: how much ‘wealth’ will go away when the shades back off?

The total value of all bitcoins known to exist is now about $2.3 trillion. But like the currency in which it is calibrated, bitcoin wealth is ghostly…spectral…unreal…and a bit scary. It appeared out of nowhere. No factory produced it. No one sweated to make it. It has no material existence of its own…and there has been no increase in the real economy to keep up with it.

At today’s prices, there is enough bitcoin wealth to buy three million houses…or 30 million F-150 pick-ups. These are real things, made by real people, working with real tools and real resources in the real economy. But they do not exist.

If investors all sold out of bitcoin in order to buy pick-ups or houses, prices of the former would go way down and prices for the latter, drawing on existing stocks, would go way up. What kind of ‘asset’ is it that loses value when you try to use it?

The value of a pick-up truck doesn’t go down when you start the engine. ‘Ghost wealth,’ on the other hand, drives away on its own.

Suppose bitcoin rose to be worth $1,000,000…with the total market cap edging up to $20 trillion. Does that imply that there are more F-150s to buy? More houses available?

Of course not. It only means that there is an additional (theoretical) $20 trillion worth of purchasing power — more bitcoin ‘wealth’ that came out of nowhere and is not supported by real output.

And it competes with the ghost wealth in stocks — now estimated, by us, at about $30 trillion. Stock prices have gone up far more than the value of the real goods and services their companies produce. This ‘ghost wealth’ cannot be turned into real wealth because, as with bitcoin, there is no equivalent in goods and services.

Even in the darkest days of 1929, real wealth — the Model T Fords, raccoon coats, and ‘carpenter vernacular’ houses — still had value.

But the ghost wealth in stocks, bid up in the Roaring Twenties, disappeared. From a low around 67 in 1921, the Dow rose to 333 in 1929. But then it collapsed by 89% over the next three years…and didn’t return to 333 again until Eisenhower was president twenty two years later.

And, in the 1990s, there was the ghost wealth in dot.com stocks, concentrated in the Nasdaq. Like bitcoin, the dot.coms looked unstoppable. The Nasdaq rose from 1,500 in August of 1998 to over 4,600 in March of 2000.

Then, the shades split town…and took their money with them. The entire gain from the previous twenty months was wiped out…with the index falling to 1,300. It took fourteen years to fully recover.

Will the same thing happen again?

Most likely.

Research Note, by Dan Denning

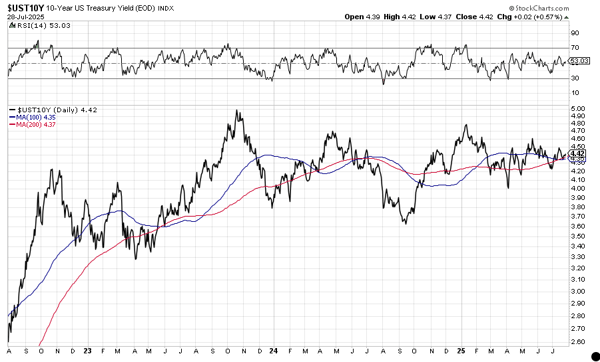

Wowee! The first borrowing estimate from the US Treasury is in since the ‘Big Beautiful Bill’ passed…and it’s uglier than expected. In a note to paid readers on Friday, I mentioned that this early Quarterly Refunding Announcement would confirm that US debt growth is out of control. It did.

Treasury said it will borrow over $1 trillion in the next three months. This is more than double what it expected to borrow just a few months ago. The announcement cited a lower cash balance in the Treasury General account (the government’s checking account, basically) and lower than expected tax receipts during the third quarter of the fiscal year.

Tomorrow we’ll learn the mix of the scheduled borrowing…bills, bonds, and notes. All eyes will be on the most important price in markets, the 10-year US government bond yield. So far, Treasury Secretary Scott Bessent has succeeded in keeping the 10-year from reaching 5%. That’s a kind of ‘red line’ in markets that triggers all sorts of other stresses—including in stocks. Stay tuned.

|