|

Perspective

By Rich Checkan

Last month, this is what I said…

“Many investors are taking a wait and see attitude.

They feel gold and silver prices are high. They are hoping for lower prices before Chairman Powell and the FOMC start raising rates (if they do) later this year.

I think that is a mistake…

… The economy is not strong right now. Gold and silver prices are not high right now.”

I hope you listened when I urged you to take action to buy gold and silver.

Gold has set new all-time highs for a closing price this week. And silver has started to keep pace with gold over the past month. The Gold/Silver Ratio (GSR) is holding steady at 88 – meaning it takes roughly eighty-eight ounces of silver to buy one ounce of gold.

If you have not taken action, do not fret… but do not delay either.

Sentiment Is Slowly Building

I have not been able to say this for quite some time, but it appears that sentiment for gold is turning positive.

Last week, I was in Ojai, California for the 26th Annual Investment U Conference hosted by The Oxford Club. I was fortunate to have four different opportunities to address the in-person and virtual attendees.

In every case, my presentations were well attended, and those in attendance were incredibly involved. They stayed to the end. They asked excellent questions.

In other words, they were eager to hear about gold.

And to be honest, that simply has not been the case over the past few years… at any of the conferences I have attended.

Reality Is Setting In

Over the past couple of years, we have seen the rate of inflation initially skyrocket to forty-year highs, then, slowly come down to more manageable levels around 3%... but still higher than the Federal Reserve’s target rate of 2%.

We have also seen interest rates explode to over 5%... after spending a decade at or near zero. Money was “free” for a long time. Then, almost overnight, money came at a price.

This has negatively affected the housing market. Refinancing has dried up to nothing. Who wants to refinance their home to move their loan interest rate from 3% to 8%? Nobody.

In addition, the combination of higher rates, tighter lending conditions, and already inflated home values have put home ownership out of reach for many.

The credit card companies are benefiting from the higher cost of goods and services. Or, more accurately, they stand to benefit if consumers can pay their credit card bills.

Time will tell whether consumers can pay down over a trillion dollars’ worth of debt at twenty plus percent interest rates. However, the rising delinquency rates suggest consumers will struggle to do so.

The Next Shoe to Fall

Given this environment, we were not surprised by the conversations we are having with clients.

In particular, one good and long-time client of ours sold some gold and silver back to us a couple of weeks ago. When he did, he apologized to us for selling his gold and silver. He promised he would get back in the market as soon as he could.

It turns out, he needed to pay off his credit card debt.

We have actually seen this unfold over the past year. Refinancing to take cash out of a home is not an option for the reason mentioned above. Credit cards were where consumers turned next to meet the shortfall between income and outgo.

The next shoe to fall is to sell an asset that is a liquid store of purchasing power to meet the financial crisis.

And yes… not being able to afford necessities constitutes a financial crisis!

Of course, the good news is that he had the means available – gold and silver – to meet his crisis head-on.

“I Can’t Afford It.”

We are hearing this more and more. We get it.

Outside of wealthy investors and central banks, nobody else has been buying gold and silver.

Most often, the reason given is, “I can’t afford it.”

My best guidance is you need to find the money somewhere because you can’t afford not to buy gold and silver here.

Alex Green, the Investment Director for The Oxford Club, gave a fantastic opening presentation in Ojai. Alex highlighted how polar opposite everyone is on various issues. He pointed out that there is no agreeing to disagree on different points of view any longer. Instead, differences of opinion are elevated to matters of right and wrong… good versus evil.

Yet, there is one major point that Democrats and Republicans both agree upon… entitlement programs like Social Security, Medicare, and Medicaid are never to be cut.

But there is one major problem with that. They make up a lion’s share of our annual federal budget, and without cutting them, we are guaranteed to continue deficit spending and growing the $34 trillion debt.

There is zero appetite by anyone in Congress – nor by either President Biden or former President Trump – to balance the budget.

This always has and always will lead to inflation (defined as the expansion of the money supply). Inflation always has and always will lead to an increase in the prices of everything that has any value whatsoever.

Find a Way

This is exactly why you must find a way to buy gold and silver… now… before the prices climb out of reach.

If you do not have your allocations of gold and silver set, set them now.

If you do not have the funds readily available in cash, find them elsewhere.

Stocks have been climbing (in dollar terms, but not in gold terms). As a result, your allocation to equities is most likely skewed higher than you planned. If so, take profits, and put the proceeds into gold and silver.

Consider using IRA funds.

If nothing else, set a small amount of money aside with each paycheck and start to accumulate your allocation over time. Every single little bit will help. Every single little bit will make a difference in your future.

There is absolutely no better way right now to Keep What’s Yours!

Buy on our website directly… www.assetstrategies.com. Call us at 800-831-0007. Or, send us an email.

You can’t afford not to.

—Rich Checkan

Editor's Note: Lobo Tiggre is the founder, CEO, and principal analyst and editor of Louis James, LLC. He researched and recommended speculative opportunities in Casey Research publications from 2004 to 2018, writing under the name “Louis James” for privacy reasons. While at Casey Research, he learned about the newsletter business from Casey co-founder David Galland, and resource speculation from the legendary speculator Doug Casey himself. Lobo will be joining us as a special guest for our next On the Move Webinar on March 27th... register today to claim your free spot.

Feature

Emotional Intelligence

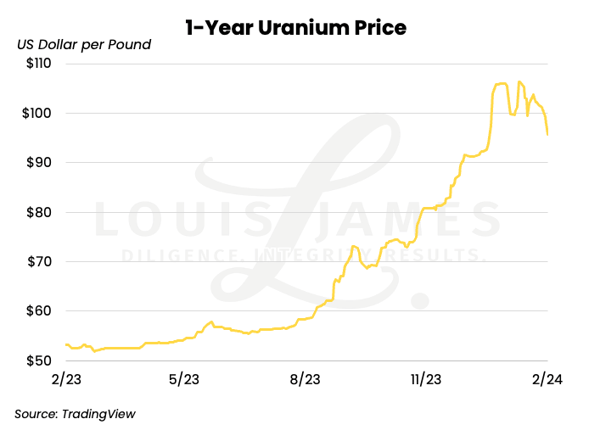

I took a lot of flak from uranium über-bulls last month for daring to say that no price can go vertical forever.

I was criticized for raining on the uranium parade during the Vancouver Resource Investment Conference uranium panel.

Like it or not, I call ‘em as I see ‘em.

It was entirely reasonable for me to say that uranium was likely to take a breather in the January 13 edition of this letter:

[J]ust look at that spot uranium chart… I don’t see how any experienced investor can see a price go vertical like that and say, “Sure, that looks sustainable.” Beware of irrational exuberance.

And I was right, of course…

This took no clairvoyance to call—only resistance to hype.

Granted, it’s still not an official correction. But let’s not quibble over semantics; uranium did not go straight to the moon as the angry über-bulls were saying. That’s significant.

A key point here is that I remained bullish and said that a correction should be seen as a buying opportunity:

If it corrects soon—which would be perfectly normal—those late to this party might just get a shot at better entry points.

I would urge anyone who doesn’t have any uranium picks in their portfolio to go for a first stake in any of the better ones they like—on the next dip, of course.

That’s because the case for uranium has only gotten better.

• Kazatomprom, the world’s largest and lowest-cost producer missed production last year and slashed its forward guidance.

• Canada’s big uranium producer, Cameco, is producing more, but has run into difficulties doing so—and is still buying on the spot market to meet its contractual sales obligations.

• The EU throwing its weight behind the push for small modular reactors (SMRs). This is a big deal. SMRs are only relatively small. Their widespread adoption would add a huge new source of demand not in anyone’s current supply–demand models.

I said all along that developments like this make any significant dip we get in this multi-decade bull market for uranium a buying opportunity.

But this wasn’t good enough for the angry über-bulls.

I was told (not always so politely) that:

• Respected source X says uranium is going straight up from here, so I must be ignorant/an idiot/lying, etc.

• Me “talking uranium down” was unnecessary and bad for the sector.

• I was wrong to say that a correction was likely weeks ago, as the price is much higher now.

• I jinxed the market.

• I shouldn’t be talking about selling when this uranium bull is just getting going.

• I’m a bear and I’m wrong.

• “It’s just a flesh wound!”

I’m sure some of the “jinx” remarks were kidding. But anyone who actually believes in such things… should probably turn their funds over to a wealth manager with a proven track record.

One person even said they sold all their uranium stocks weeks ago because of my bearishness and missed out on the rally to triple digits. I’m sorry for this person, but I do not accept responsibility for an individual’s emotional overreaction in contradiction of what I actually said.

And no one goes broke taking profits.

For the record:

• I’ve never said to sell everything in this space.

• My outlook for uranium has been, is, and remains bullish for years, if not decades to come.

• Pointing out the probability of corrections along the way does not change this.

• I’ve never claimed I could time market corrections.

• I’ve been saying since last November that despite the market being ripe for correction, there’s potential for uranium to become the flavor of the day (FOTD) and for spot prices to go much higher than the fundamentals justify.

• In recent interviews, I’ve said that either for geopolitical reasons or a FOTD mania, uranium could go to $150 or higher by this summer.

• I have taken some profits, but that doesn’t make me a traitor to some sacred cause; it makes me a rational actor in a market where prices can crash without warning (if there’s a major nuclear incident).

• I own more uranium stocks than I ever have in the past.

• I am nowhere near influential enough to affect uranium prices and have little impact on company share prices.

• The main thrust of my remarks has not been to encourage those long to sell, but to discourage those looking to go long from chasing stocks near 52-week or multi-year highs.

My reason for writing about this, however, is not to defend my wounded pride.

The value here is in looking at the psychology at play.

I understand that having a lot of money riding on a speculation makes it difficult to read “negative press” with equanimity.

That doesn’t make it reasonable for über-bulls to get angry at me for saying that a normal, healthy correction was likely—especially when I was saying it would be an opportunity.

Some felt a need to disparage my character and my work. In my view, this says more about them than me.

The important thing is that this sort of emotional response is not conducive to positive investment outcomes for them.

It’s fine to be a bull, but dangerous to be one blinded by rage: there’s a sword behind the red cape.

If one heaps hate on anyone who disagrees with a favored investment thesis—or just tunes them out—one increases the chances of being blindsided by the unexpected. Bulls in echo chambers don’t see the butcher coming.

Simply understanding this—and the value of thoughtful challenges to one’s investment ideas—can help one achieve more positive investment outcomes… or at least avoid some wipeouts.

I don’t mean to sound insulting or condescending, but there’s a great deal of literature and help out there for anyone who struggles with anger management, blame-shifting, and other such issues. We’re not all born with nerves of steel and the discipline to seek truth over confirmation, but it’s possible to train ourselves in that direction.

I speak from personal experience.

And I sincerely hope these remarks will motivate some folks to introspect and embrace change—for the sake of their portfolios, not mine… and perhaps even more important things in Life.

P.S. If you missed this guidance before uranium corrected, be sure to sign up for my free, weekly, no-hype, no-spam Speculator’s Digest.

Editor's Note: Frank Holmes is the CEO of U.S. Global Investors —a company that produces quality analysis concerning gold, precious metals, natural resources, and emerging markets—in conjunction with his work as a fund manager. Frank is a long-time friend of ours, and we've chosen to share his article originally published March 1, 2024. For more articles like this from Frank and other leading experts, you can subscribe to the U.S. Global Investors newsletter here.

Hard Stuff

The Surge In Bitcoin ETFs And Its Potential Impact On Gold

By Frank Holmes

Bitcoin and gold were both top of mind at this past week’s 2024 Investment U Conference in Ojai, California, which I had the privilege of presenting at.

There was a rumor circulating that the Bitcoin price rally was sparked by a large financial institution recommending a 2% to 3% weighting to some of its high-net-worth clients. I can’t confirm this, but it’s being reported that Bank of America and Wells Fargo are now offering the Bitcoin ETFs to certain wealth management clients, joining Charles Schwab, Robinhood and others.

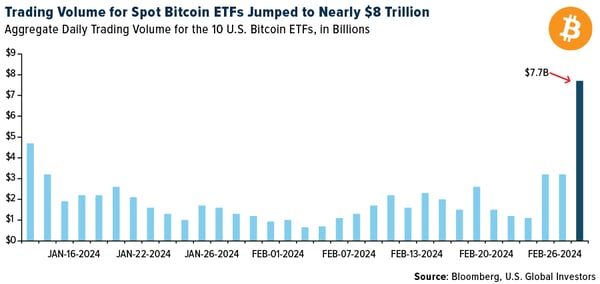

The price of Bitcoin pumped more than 45% last month, with around half of those gains recorded in the final week, as demand for the long-awaited spot Bitcoin ETFs hit a fever pitch. Combined daily trading volume for the 10 ETFs was a jaw-dropping $7.7 billion on Wednesday alone, fueled by institutional speculation and leveraged bets that pushed the price of the underlying asset to a near-record high.

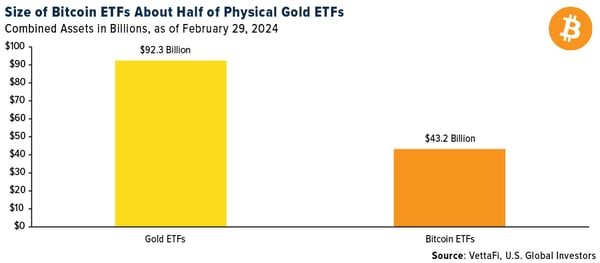

Remarkably, as of February 29, the combined value of the holdings in U.S.-based Bitcoin ETFs was roughly half the value of all known gold ETFs. The Bitcoin ETFs, which began trading in January, held $43.2 billion, while gold ETFs held $92.3 billion.

The cryptocurrency’s breathless catch-up to gold is reflected in the dramatic difference in sentiment between the two assets right now. CoinStats’ Crypto Fear and Greed Index is currently flashing Extreme Greed, while JM Bullion’s Gold Fear and Greed Index sits in Neutral territory.

A Tale Of Two Assets: Risk And Reward

As you know, I often recommend a 10% weighting in gold, with half in physical gold (coins, bars, jewelry) and the other half in high-quality gold mining stocks, mutual funds and ETFs. I believe this weighting is suitable for most investors seeking a non-correlated asset, but especially conservative investors who might not have a long-term investment horizon.

For investors with a longer horizon, or those with a bigger risk appetite, there’s Bitcoin, whose volatility is about eight times greater than that of gold, its analog cousin. Whereas the precious metal has a 10-day standard deviation of ±3%, Bitcoin’s is ±25%.

Though not guaranteed, with greater risk can come greater reward. For the six-month period through the end of February, Bitcoin more than doubled in price, surging close to 130%. Over the same period, gold increased a little over 5% while gold majors, as measured by the NYSE Arca Gold Miners Index, lost 9%.

Whether the excitement surrounding Bitcoin is siphoning flows away from gold is unclear, but there does appear to be some disconnect between gold’s price action and investment levels. Historically, the gold price and holdings in gold-backed ETFs have traded in tandem, but starting in 2023, the two began to decouple, as you can see below. This could be caused by a number of factors, including changes in investor sentiment, monetary policy, portfolio balancing, currency fluctuations and more.

Gold Was Up, But Most Miners Couldn’t Grow Free Cash Flow

Analysts here at U.S. Global Investors looked at a basket of 85 gold mining stocks and found that, generally speaking, financial conditions worsened for the industry in 2023, despite the fact that gold had a relatively good year, jumping more than 13%.

Our analysis shows that, of those 85 names, only 47—or 55% of the basket—reported a positive free cash flow (FCF) yield as of December 31, 2023. That’s little changed from a year earlier, when 48 gold producers had positive FCF.

The same concerning results surfaced when we compared sales growth to changes in the price of gold. In December 2022, 23 out of 85 gold miners had positive FCF as well as sales growth that outpaced the yellow metal over the trailing 12 months (TTM); a year later, that figure fell to 10, representing only around 12% of the basket.

This means that fewer than one in 10 gold miners recorded an improvement in financial conditions…during a year when the price of gold was up.

For this reason and more, younger people just haven’t shown interest in gold stocks, which is a shame for the companies. We’re on the verge of history’s greatest transfer of wealth, with $84 trillion expected to be left to heirs over the next two decades. Perhaps producers should take a page out of Bitcoin miners’ playbook and HODL their gold.

Will Central Banks Start Buying Bitcoin?

As I shared with you, some market watchers, including our shop, have noted that the driver of the gold price appears to have shifted in recent months. For decades, the yellow metal had an inverse relationship with real rates—rising when yields fell, and vice versa—but since the start of the pandemic in 2020, this pattern has broken down. During the 20 years before the pandemic, gold and real rates shared a highly negative correlation coefficient. Since that time, though, the correlation has turned positive, and the two assets now move in the same direction more often than not.

BMO Capital Markets commented on this in January, making the case that buying activity by central banks is the new driver of gold. It’s hard to argue against this position. Financial institutions, chiefly those in emerging economies, have been net buyers of the metal since 2010 in an effort to support their currencies and diversify away from the U.S. dollar.

For what it’s worth, Edward Snowden shared his 2024 prediction this week that a national government will be found to have been secretly buying Bitcoin, “the modern replacement for monetary gold,” the former NSA whistleblower said in a tweet.

This would be something, though I should point out that the government of El Salvador currently holds 2,381 bitcoins in its treasury. Its president, Nayib Bukele, says these holdings are up 40% after the recent price rally, and yet he has no intention of selling. El Salvador and the Central African Republic (CAR) are the only two countries so far that have made Bitcoin legal tender.

Editor's Note: Nomi Prins is a best-selling author, financial journalist, and former global investment banker. At Rogue Economics, Nomi shines a light on the collusion that happens between Wall Street and Big Government behind closed doors, and she provides actionable steps for readers to protect and grow their wealth. This article was originally published on February 19, 2024. Click here to discover more of Nomi's insights.

The Inside Story

The NYCB Saga Isn’t Over Until the Fed Sings

By Nomi Prins

The Federal Reserve has a history of sweeping mounting loan problems under the rug – until the rug gets pulled. The S&L crisis in 1989, which struck at the heart of the savings and loan industry, is one case. The budding subprime mortgage crisis that led to the full-blown financial crisis of 2008 – which former Fed Chair Ben Bernanke repeatedly denied would happen – is another.

Enter current Fed Chairman Jerome Powell and the budding commercial real estate loan crisis.

It’s been a year since the Silicon Valley Bank meltdown triggered a regional banking crisis.

And we are on the brink of another one. Let me explain.

You may have seen the headlines about New York Community Bancorp’s (NYCB) recent 60% stock plunge. Its shares hit a new low before rebounding the morning Moody’s downgraded its credit rating to junk status.

Let me put that in context. Because you might not know that NYCB took over $38 billion of Signature Bank’s assets after it failed last March.

You see, that purchase made NYCB bigger. As a result, NYCB popped into a higher regulatory category – meaning it had to have more capital set aside in case of a financial emergency.

Only it doesn’t. That’s why its mounting recent commercial real estate (CRE) losses mean it could eat through the capital it does have. Hence, Moody’s downgrading its rating on February 8.

Let me unpack that further. At its recent earnings call, NYCB reported $252 million in losses for Q4 2023, mostly in CRE. That’s mainly because the office vacancy rate in New York City hit 17% at the end of 2023. That’s a record high.

Higher office vacancies mean less money coming in to pay for commercial office real estate loans. That causes delinquencies or defaults in payments. Throw in the fact that rates have been higher due to the Fed’s tightened policy, and it accelerates budding problems with paying loans.

Unfortunately, this is a growing trend across many major U.S. cities.

Chicago, San Francisco, and Houston are all facing rising office vacancy rates above 20%.

That means associated CRE values are falling, and loan payments aren’t getting paid. And that plagues regional banks in those cities and other cities where office vacancy rates are rising.

The harsh reality is this. As long as rates stay high, regional banks will face more problems with CRE and other loans. They don’t have the luxury of diversifying assets like larger banks do to ride out such storms.

Plus, according to Goldman Sachs research, roughly $1.2 trillion in commercial mortgages are due to mature in 2024 and 2025. They might be rolled into new mortgages at higher interest rates. Or, if borrowers can’t afford that, it forces sales in underlying properties. This also means less money coming into loans as payments. So, this problem isn’t going away anytime soon.

The Fed’s Demolition Project

The Fed began raising rates in March 2022. Since then, regional banks have faced mounting challenges.

But I’d like to highlight the key reasons and the connection between tighter Fed policy and problems in the banking system.

1. Higher Interest Rates. More expensive money leads to a decrease in borrowing and lending activity. When rates rise, it’s more expensive for individuals and companies to get and pay interest on loans. As a result, credit demand for loans drops.

2. Increased Cost of Borrowing. On top of reduced loan demand, regional banks have faced higher borrowing costs. As rates rise, banks need to pay higher interest to depositors, which cuts into their profit margin. So regional banks need to raise interest rates on their loans, making them less attractive as opposed to larger banks that have greater access to the Fed for money they borrow.

3. Liquidity Challenges. Regional banks use short-term funding to meet their financial obligations more than larger banks. That liquidity can come from deposits or borrowing from the Federal Reserve. When rates rise, it’s more expensive for them to access this. The resulting liquidity crunch can cause problems in meeting their financial obligations.

Regional Banks in the Eye of the Fed Policy Storm

Regional banks focus on the financial needs of individuals and businesses in certain geographic areas. (National or international megabanks such as JPMorgan Chase or Citigroup have a broader scope).

That means any economic or financial event impacting the area can have an outsized effect on related bank loans. That’s what happened with NYCB.

But the problems in the regional banking sector today are not confined to one area. They are a net result of higher loan costs driven by higher interest rates and faltering commercial real estate.

That’s why we are seeing their stock prices hit across the country.

So while the media focused on the share price collapse of New York Community Bancorp, numerous other banks are trading at or near their lowest levels in two years.

It’s not a pretty picture in the regional bank arena, whether for banks operating in many states or a few…

U.S. Bancorp, the parent of U.S. Bank, is the 5th largest bank in the U.S., with about $663.5 billion in assets. It operates in 28 states. Its stock has shed 30% of its value in the past two years.

KeyBank is the 22nd largest bank in the U.S. with $186 billion in assets. It operates in 16 states. And its stock has lost 50% of its value over the past two years over the same issues.

Zions Bank stock has lost about 42% of its value since the Fed began raising rates. It has a high concentration of commercial real estate exposure relative to the amount of capital it holds. And it has high office space exposure.

Small regional banks have felt even more intense pain. First Foundation Inc., the parent of First Foundation Bank, has seen its share price plummet by 70% in two years. It operates in California, Nevada, Florida, Texas, and Hawaii.

Broader Commercial Real Estate Turmoil

Now, small banks account for nearly 70% of all CRE loans outstanding in the U.S. That figure includes loans made by these banks and loans they purchased from larger banks.

As Fitch Ratings notes, “Banks with less than $100 billion in assets possess higher CRE concentrations than their larger counterparts.”

That’s why losses in that category “could result in the failure of a moderate number of smaller banks.”

It gets worse. According to MSCI Real Assets, about $85.8 billion of U.S. commercial property debt was distressed at the end of 2023. And there’s an additional $234.6 billion of debt in potential distress.

Commercial property prices are down 21% from their March 2022 peak. And within that sector, office prices showed the biggest drop – falling by 35%.

Banks hold $441 billion of commercial property debt coming due this year out of a total of commercial property loans coming due of $929 billion, And about $234 billion of that maturing debt held by banks is securitized in CMBS, collateralized loan obligations, and asset-backed securities.

Fitch reported that if commercial property prices decline by approximately 40%, losses in CRE portfolios could ignite the failure of a “moderate number” of predominately smaller banks. Some regional banks could be forced to sell loans at a loss or increase provisioning for losses.

Careless Powell

It’s easy not to care about things like regional or local bank failures when you’re breathing the rarefied air of power and job security. Maybe that’s why Fed Chair Jerome Powell didn’t bat an eye when asked about the commercial real estate market’s impact on banks.

“It feels like a problem we’ll be working on for years,” he told CBS in a 60 Minutes interview.

He admitted that “it’s a sizable problem.” Then he said it was a “manageable one” and confirmed it was more likely to impact smaller or regional banks.

Gee, thanks, Jerome. Last June, a few months after the collapse of Silicon Valley Bank, then the second largest in U.S. history, Powell said he was keeping an eye on CRE and ramifications on the U.S. banking system. And yet, here we are – with so many measures of loan stress rising.

Now, his use of the word “manageable” was interesting to me. It’s like all Fed Chairs use the same song lyrics. That was the same term Treasury Secretary (and former Fed Chair) Janet Yellen used in her testimony to the House when asked about brewing CRE problems.

This was during one of two testimonies she gave that week – one to the Senate and one to the House – on the U.S. banking system.

She downplayed CRE risks. She told the House Financial Services Committee on February 8 that she was concerned about stresses in CRE but that the situation was “manageable.”

As I said earlier, I don’t trust Fed or former Fed officials when they say things are manageable or not really problems. Especially when it comes to loans and banks. Not when the data suggest otherwise.

That’s why I suggest you avoid investing in any regional banks for now.

|